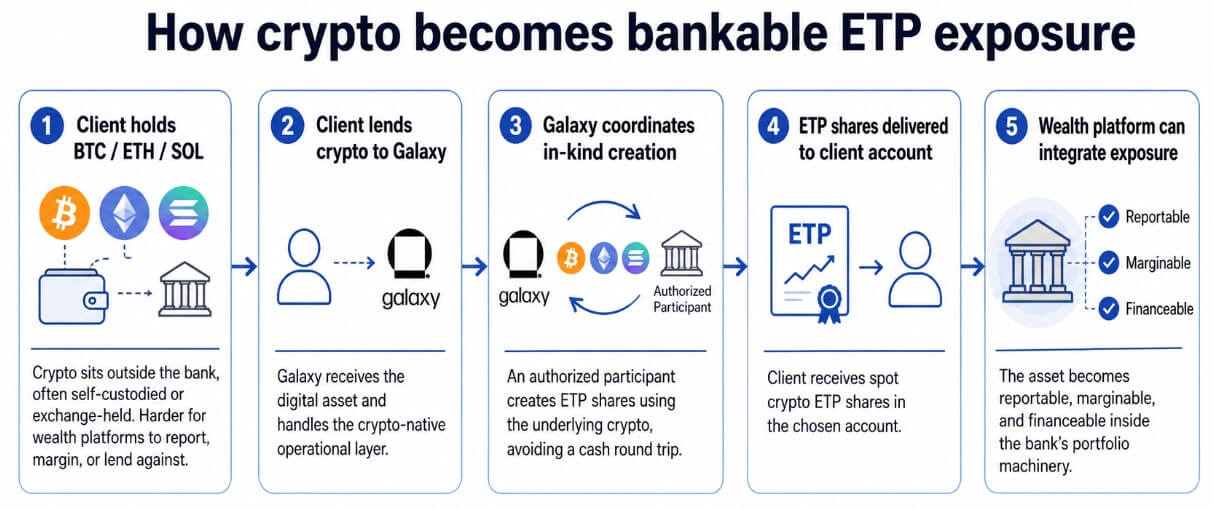

Morgan Stanley introduced on June 5 that eligible wealth administration purchasers can now lend Bitcoin, Ethereum, or Solana to Galaxy Digital and obtain shares of spot crypto exchange-traded merchandise in return.

Galaxy will coordinate an in-kind creation with a certified participant, then ship ETP shares instantly into the consumer’s chosen account. Onboarding timelines that beforehand exceeded 4 weeks might fall by as much as 75%.

For Morgan Stanley-referred purchasers, Galaxy has lowered the minimal transaction dimension from $25 million to $5 million.

US-traded spot Bitcoin ETFs recorded a historic $4.4 billion in internet outflows over 13 consecutive weeks, extending into early June. Bitcoin has fallen roughly 53% from its October 2025 all-time excessive close to $126,200 and briefly touched $60,000 this week.

Towards that backdrop, Morgan Stanley’s association provides wealth purchasers direct holding of cash that enter the financial institution’s portfolio equipment and change into marginable, reportable, and accessible to the identical infrastructure that already helps securities lending, margin accounts, and personal banking.

The regulatory layer that made this doable

The SEC’s approval of in-kind creations and redemptions for crypto ETPs in July 2025 eliminated the central structural impediment.

That change permitted approved contributors to create and redeem spot crypto ETP shares utilizing underlying crypto property, transferring the plumbing nearer to how commodity ETPs already operate.

Galaxy can now take a consumer’s BTC, use it to create ETP shares in variety, and ship these shares and not using a taxable sale of the underlying asset, a workflow that may have required a money conversion spherical journey beneath the prior guidelines.

Morgan Stanley limits its function to referrals and consumer schooling, and Galaxy supervises onboarding and bears the crypto operational publicity.

That division retains Morgan Stanley on the regulated-securities facet of the interplay, whereas Galaxy bears the operational publicity to crypto.

Exterior crypto wealth, beforehand held in self-custody or on an alternate, strikes right into a bankable portfolio, the place it could actually function collateral for margin and combine with reporting and lending providers.

Three fashions for 3 theories

Morgan Stanley’s association sits inside a broader institutional divergence about which type of crypto publicity banks can safely acknowledge, and three fashions at the moment are operating in parallel.

The primary is ETP collateral, which is essentially the most bank-friendly kind, since banks perceive find out how to value, custody, margin, and liquidate a registered safety. JPMorgan moved right here first, accepting BlackRock’s IBIT shares as collateral for loans earlier than increasing additional.

The Morgan Stanley/Galaxy association extends this mannequin by changing crypto held outdoors the financial institution into ETP shares that slot into current wealth-management, margin, and lending workflows.

The second mannequin is direct crypto collateral, representing the larger structural leap. JPMorgan deliberate to permit institutional purchasers to pledge BTC and ETH instantly towards loans by year-end 2025, with third-party custodians holding the pledged property. The financial institution has not publicly confirmed a reside product, and the standing remains to be primarily based on reported plans.

| Mannequin | Financial institution consolation degree | Principal asset kind | Instance from article | What banks like | Principal threat |

|---|---|---|---|---|---|

| ETP collateral | Excessive | Spot Bitcoin / crypto ETP shares | Morgan Stanley/Galaxy; JPMorgan accepting IBIT collateral | Acquainted securities wrapper, custody, pricing, margining | ETF outflows transmit institutional promoting |

| Direct crypto collateral | Medium to low | BTC / ETH pledged instantly | Reported JPMorgan BTC/ETH collateral plan | Extra direct use of crypto as balance-sheet collateral | Volatility, custody, margin calls, liquidation rights |

| Tokenized collateral substitution | Rising | Tokenized Treasuries, MMFs, deposits | Customary Chartered/OKX/BlackRock BUIDL; HSBC tokenized deposits | Yield-bearing, lower-volatility collateral leg | Settlement, authorized, and platform interoperability threat |

If operational, it will deal with BTC and ETH the way in which banks already deal with publicly traded shares in a margin account, with real-time valuation, haircuts, and automatic margin calls.

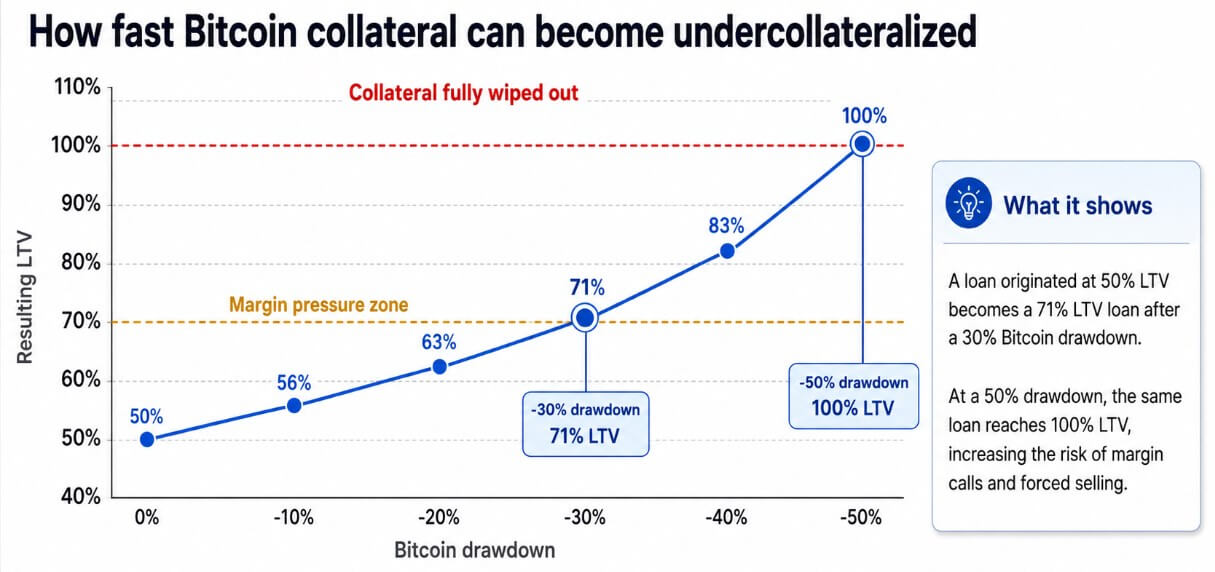

A mortgage originated at 50% loan-to-value turns into a 71% LTV mortgage after a 30% Bitcoin drawdown. At a 50% drawdown, that very same mortgage hits 100%, leading to full collateral wipeout.

The $1.8 billion in compelled crypto liquidations recorded on June 3 alone, the most important single-day determine since February 2026, illustrates what leverage produces in a quick market.

The third mannequin, tokenized collateral substitution, could show to be essentially the most sturdy. Banks choose tokenized Treasuries or cash market funds because the collateral leg, whereas crypto stays because the traded threat asset.

On Apr. 28, OKX, BlackRock, and Customary Chartered launched a framework that permits institutional purchasers to put up BlackRock’s BUIDL tokenized Treasury fund as yield-bearing margin collateral on OKX, with Customary Chartered serving as the primary G-SIB custodian in such an association.

Purchasers earn yield on collateral they might in any other case go away idle, and Customary Chartered handles regulated off-exchange custody, holding property segregated from the alternate’s personal holdings.

What banks are literally constructing

Customary Chartered’s off-exchange mannequin with OKX means crypto-native buying and selling venues want a regulated G-SIB wrapper to draw essentially the most cautious institutional capital.

BNY is constructing its digital asset platform by combining custody, collateral administration, financing, funds, and 24/7 liquidity rails, positioning it because the infrastructure substrate on which crypto lending and tokenized asset markets will run.

Citi has framed its function round settlement, custody of stablecoin reserves, and crypto ETF custody providers, claiming the plumbing.

Each main financial institution is competing to manage the wrapper, the custodian, the collateral agent, or the servicing infrastructure via which Bitcoin flows.

Two paths via the identical plumbing

Within the bull case, regulatory readability and stronger custody controls normalize the usage of BTC and ETH as pledged collateral for institutional debtors.

Citi’s June 2026 tokenization report places international tokenized property at roughly $17 billion at the moment, with a 2030 bull-case forecast of $8.2 trillion.

If that trajectory holds, crypto collateral turns into a routine characteristic of financial institution lending, tokenized Treasuries develop as the popular institutional margin asset, and Bitcoin turns into extra helpful as a balance-sheet instrument.

The plumbing that Morgan Stanley and Galaxy are assembling will get prolonged throughout non-public banking at scale, pulling self-custodied wealth into managed portfolios the place it may be financed, reported, and deployed.

Within the bear case, volatility and operational threat hold banks anchored to the ETP wrapper. Direct Bitcoin collateral applications keep narrowly eligible and high-haircut, with restricted attain past a slender institutional base.

Banks lean on tokenized Treasuries and deposits, with HSBC increasing its tokenized deposit service to US purchasers in April 2026, enabling 24/7 on-chain fund motion with out public-chain settlement threat, whereas uncooked BTC lending stays confined to a small set of crypto-native lenders and hedge funds.

Bitcoin ETF outflows change into a recurring characteristic, for the reason that regulated wrapper attracts capital that additionally leaves via the identical door when sentiment shifts.

The leverage loop

Neither state of affairs eliminates the structural consequence of collateralization itself.

Galaxy Analysis estimated that crypto-collateralized lending reached $73.59 billion within the third quarter of 2025, break up amongst DeFi lending (55.7%), CeFi (33.1%), and crypto-collateralized stablecoins (11.2%).

As banks increase from ETP collateral towards direct BTC and ETH lending, extra of Bitcoin’s value conduct will mirror institutional deleveraging cycles.

The $4.4 billion in spot ETF outflows that pushed Bitcoin beneath $60,000 this week present how shortly regulated wrappers can transmit institutional promoting. Add direct crypto-backed mortgage margin calls to that mechanism, and drawdowns carry extra compelled promoting than the market has traditionally processed.

Morgan Stanley’s association with Galaxy is a wealth-management funnel: outdoors crypto wealth enters the financial institution’s portfolio equipment, turns into financeable and reportable, and turns into extra correlated with no matter causes institutional traders to cut back threat.

Bitcoin adoption turns into built-in into the identical collateral loops that govern each different asset class, with all of the structural upside and deleveraging publicity that entails.