Final week, an institutional investor executed the biggest single off-exchange commerce within the historical past of US spot Bitcoin exchange-traded funds, offloading a $1.26 billion place in BlackRock’s iShares Bitcoin Belief (IBIT).

Whereas the transaction has sparked intense debate on Wall Avenue, an evaluation from NYDIG suggests the sale was a focused, pressing retreat by a whale reasonably than the routine closure of a well-liked hedge fund arbitrage play.

In line with the evaluation, the entity paid a steep value for fast liquidity. It incurred practically $30 million in execution prices simply to safe an exit earlier than the broader digital asset market took a notable downturn.

Understanding the IBIT megatrade

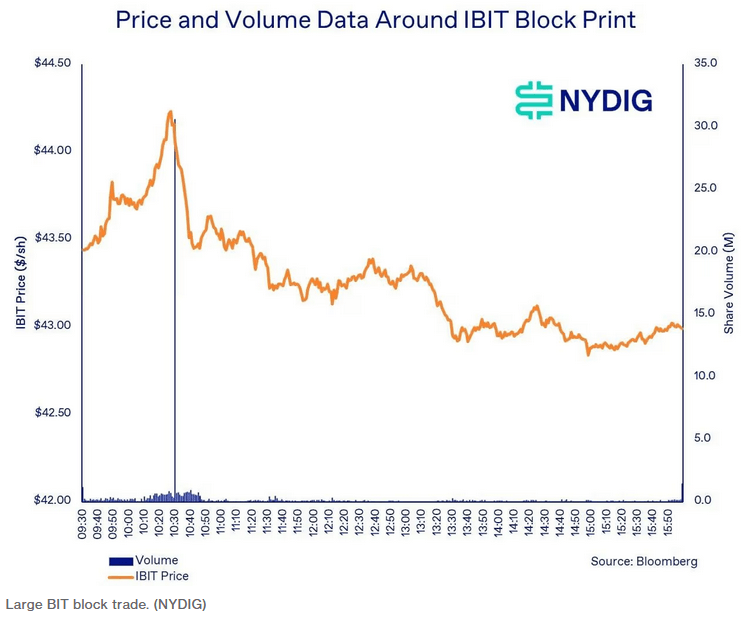

NYDIG famous that exercise in BlackRock’s IBIT started to quietly speed up following an early-morning session with regular quantity.

In line with the agency, the ETF’s share value edged upward from $43.81 to an intraday peak of $44.24 between 10:16 a.m. and 10:28 a.m. Jap Time. Buying and selling quantity throughout this window surged to 3 or 4 instances its regular fee, suggesting an executing dealer was testing market liquidity and thoroughly priming the tape for an enormous placement.

Then, at exactly 10:30 a.m., the hammer fell.

A single vendor dumped 29.21 million shares of IBIT in a privately negotiated, off-exchange transaction. The block cleared at $43.16 a share. As a result of the prevailing open-market value at that very second was $44.17, the vendor accepted a 2.3% haircut on the spot. In greenback phrases, that execution penalty price the mysterious entity roughly $29.5 million.

Regulatory reporting codes connected to the commerce illustrate the vendor’s singular give attention to velocity. The transaction was printed to the FINRA/Nasdaq TRF Carteret, which is a facility utilized by broker-dealers to report darkish pool and privately negotiated trades.

Moreover, it carried an Intermarket Sweep Order designation alongside a Reg NMS trade-through exemption.

In plain English, these exemptions permit institutional gamers to bypass the requirement of looking for the best possible displayed value throughout a number of public exchanges, supplied they take accountability for satisfying sure protected quotes.

This exhibits that the vendor actively selected the knowledge of an instantaneous, unified exit over the potential of a greater value.

Debunking the arbitrage fantasy

When extremely uncommon, billion-dollar prints happen in crypto ETFs, market commentators sometimes default to a standard rationalization: the premise commerce.

This standard hedge fund technique entails shopping for a spot ETF whereas concurrently shorting Bitcoin futures to reap the yield from the worth unfold between the 2.

Nonetheless, NYDIG’s evaluation identifies three distinct components that dismantle the basis-unwind principle on this occasion.

First, the fundamental economics don’t align. A foundation dealer depends on capturing a slim proportion yield over time. Accepting an instantaneous 230-basis-point loss on the spot leg of the commerce would immediately vaporize an enormous portion of the technique’s anticipated annual return.

Until going through a catastrophic margin name, an arbitrage desk would naturally unwind its place passively over days or even weeks to protect capital.

Second, the commerce’s structural urgency is solely misaligned with delta-neutral administration. Intermarket sweep orders and hefty block reductions are the hallmarks of a distressed or deeply convicted directional vendor, not a market-neutral yield farmer.

Lastly, the futures market supplied the final word smoking gun. A 29.21 million-share block in IBIT equates to roughly 18,500 Bitcoin. If an arbitrageur have been exiting a delta-neutral place of that magnitude, they would want to concurrently purchase again roughly 3,700 Bitcoin futures contracts on the Chicago Mercantile Alternate (CME) to flatten their e book.

Nonetheless, the CME order e book barely registered a pulse on the day. In the course of the actual minute the ETF block crossed the tape, solely 91 futures contracts modified arms. Over the complete half-hour window surrounding the commerce, barely 1,000 contracts have been executed.

Furthermore, a real foundation unwind of this dimension would have required absorbing practically half of the CME’s whole day by day quantity straight away, which might have triggered an enormous, extremely seen spike in futures exercise.

So, the overall absence of such a spike confirms the vendor was merely lengthy on Bitcoin and all of a sudden wished out.

Who’s the whale?

The sheer scale of the transaction leaves a remarkably quick listing of suspects.

NYDIG famous that the block commerce exceeded the overall holdings of all disclosed 13F traders within the first quarter of 2026, excluding licensed contributors and market makers, who maintain stock strictly for liquidity provision reasonably than funding functions.

Following a commerce of this magnitude, analysts naturally look to fund flows to trace the aftermath. IBIT recorded $192 million in web redemptions on Could 26, adopted by an extra $528 million on Could 27.

Nonetheless, market mechanics recommend these figures don’t characterize the direct, fast settlement of the whale’s shares.

As a result of the ETF’s web asset worth closed at $42.95 on the day of the commerce and at $42.43 the next day, which is properly under the negotiated $43.16 block-execution value, the counterparty that bought the shares had no financial incentive to right away redeem them with the issuer.

Doing so would have locked straight away loss. As an alternative, the customer seemingly absorbed the block into stock and has been systematically distributing the shares into the secondary market over time.

So, the final word id of the vendor and their motive stay shrouded within the opacity of off-exchange buying and selling. It’s not possible to definitively show whether or not the whale was pressured out by strict inner threat limits or whether or not they made a discretionary wager that the crypto market was headed for a sustained downturn.

Market headwinds and institutional fatigue

Following the commerce on Could 26, Bloomberg ETF analyst Eric Balchunas claimed the “market absorbed the sale properly.”

Nonetheless, the timing of the billion-dollar retreat proved proactive, as Could was a bruising month for digital property. Information from CoinGlass confirmed that the highest crypto shed practically 4% over the month, buying and selling close to $73,000 on the finish.

This value efficiency was exacerbated by the collapse in investor urge for food for spot Bitcoin ETFs.

NYDIG famous that the US funds entered the Could 26 session already nursing a six-day streak of consecutive outflows. The sector bled $1.55 billion throughout that stretch alone, with BlackRock’s IBIT shouldering the brunt of the injury, shedding roughly $1.1 billion.

By the shut of Could, the injury had compounded. The US-listed spot Bitcoin ETFs hemorrhaged $2.4 billion in whole month-to-month outflows, in line with knowledge from SoSoValue.

The sustained promoting stress dragged whole property underneath administration throughout the ETF class from north of $100 billion all the way down to $94.17 billion.