Banks are more and more turning to tokenized deposits as they undertake blockchain know-how to enhance how cash strikes by way of the monetary system. A brand new report from Arkham Intelligence says regulated banks are creating digital variations of buyer deposits that keep on the banks’ stability sheets whereas working on blockchain networks.

This transition helps banks make transactions quicker and extra automated with out disrupting the important structure of typical banking. In distinction to stablecoins, tokenized deposits stay liabilities of the financial institution and are regulated underneath banking rules.

What Tokenized Deposits Truly Do

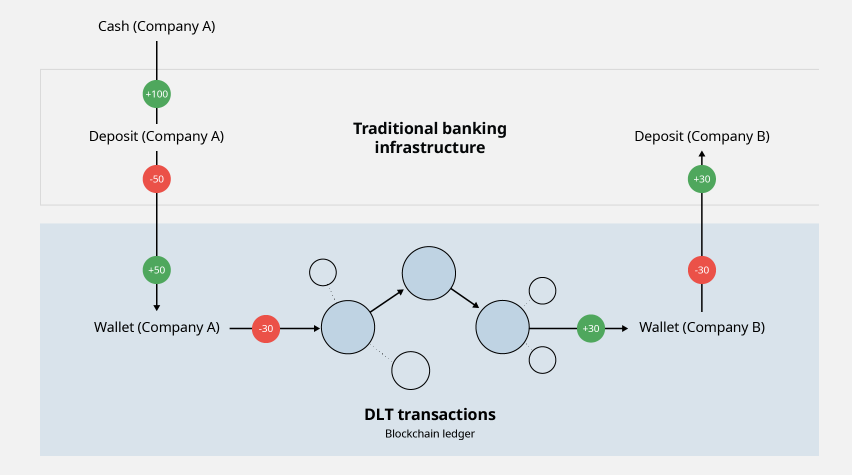

Tokenized deposits are digital variations of financial institution deposits that run on blockchain networks. Whereas the deposits stay with regulated banks, prospects obtain digital tokens that characterize the identical worth. This lets banks and companies transfer cash quicker than conventional fee methods, which regularly rely upon banking hours and take longer to settle transactions.

The know-how additionally permits banks to automate funds based mostly on pre-agreed situations. For instance, an organization can switch funds between its subsidiaries at any time or launch funds mechanically after an bill is authorized or a liquidity goal is reached.

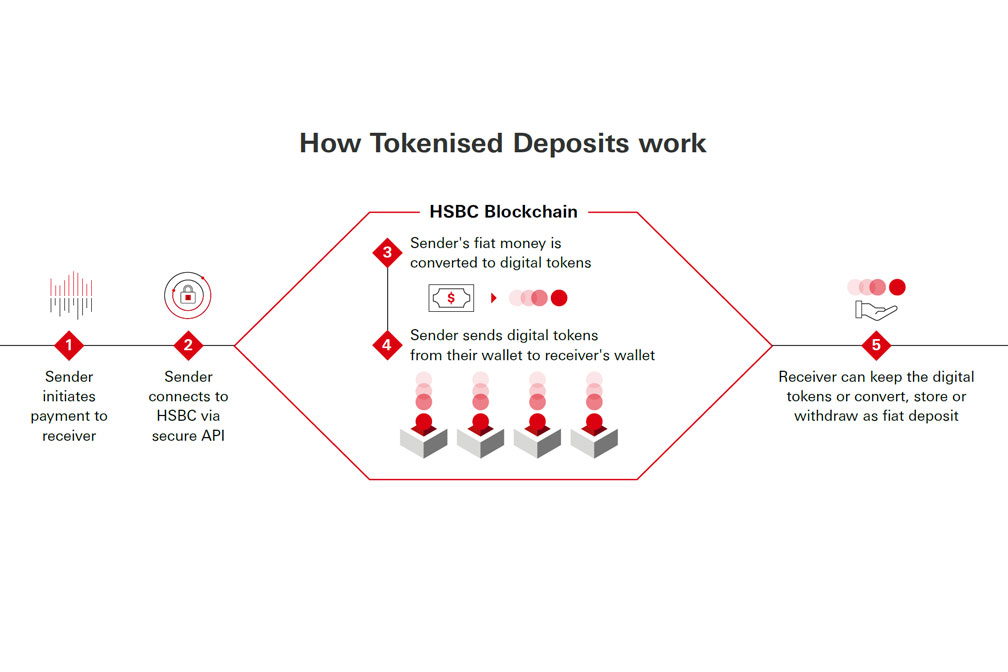

HSBC demonstrated how the know-how works in September 2025 when it accomplished its first cross-border tokenized deposit transaction between Hong Kong and Singapore for Ant Worldwide. The transaction diminished delays attributable to completely different time zones and helped the corporate handle its treasury operations extra effectively.

Why They Differ From Stablecoins

Tokenized deposits are sometimes in contrast with stablecoins as a result of each use blockchain know-how to maneuver digital cash. Nonetheless, Arkham Intelligence mentioned the 2 work very in a different way.

Stablecoins equivalent to USDT and USDC are issued by non-public firms that again their tokens with reserve property. The overall excellent provide of USD-backed stablecoins thus far has climbed to nearly $300 billion by mid-2026, in line with information from rwa.xyz.

Tokenized deposits, in contrast, are issued by regulated banks and characterize buyer deposits already held by these establishments. They’re additionally out there solely to authorized shoppers by way of permissioned blockchain networks.

A report dated February 2026 by the New York Fed emphasised that stablecoins are supposed to perform as “secure cash,” whereas tokenized deposits will probably be a part of the traditional banking system and assist with financial institution loans.

Main Banks Push Trade Adoption

Huge international monetary establishments have launched tokenized deposits methods as they proceed to undertake blockchain know-how. Among the large gamers within the trade embrace JPMorgan through its Kinexys system that was previously referred to as Onyx. The Kinexys system has performed greater than $7 billion value of transactions every day with over $3 trillion being processed from its inception.

HSBC has prolonged its tokenized deposits to the areas of Hong Kong, Singapore, UK, Luxembourg, and US. The system presents assist for various currencies and permits for automated fee and settlement of tokenized deposits.

One other participant who joined the trade in January 2026 is BNY Mellon with the launch of its tokenized deposits product concentrating on establishments. It has additionally invested in blockchain infrastructure whereas endeavor tasks associated to tokenized cash market funds.

Challenges Nonetheless Want Options

Regardless of the rising reputation of tokenized deposits, the know-how faces some hurdles. Platforms are at present being run inside one financial institution’s ecosystem, and tokenized deposits can’t be transferred from one monetary establishment to a different with out leaving the system. So as to clear up this downside, The Clearing Home intends to introduce a standard community for tokenized deposits by the primary half of 2027.

The Worldwide Financial Fund mentioned the affect of tokenization is prone to lengthen far past funds. Tobias Adrian, Director of the IMF’s Financial and Capital Markets Division, mentioned future coverage selections will decide whether or not tokenization makes the monetary system extra environment friendly or creates new fragmentation.

Associated: $60B Tokenized RWA Market Exhibits No On-Chain Exercise, Report Finds