This can be a section from the Ahead Steering publication. To learn full editions, subscribe.

This week is likely one of the greatest we’ve had shortly for financial knowledge releases.

Within the spirit of all this knowledge, let’s run by way of some charts and takeaways.

JOLTS report

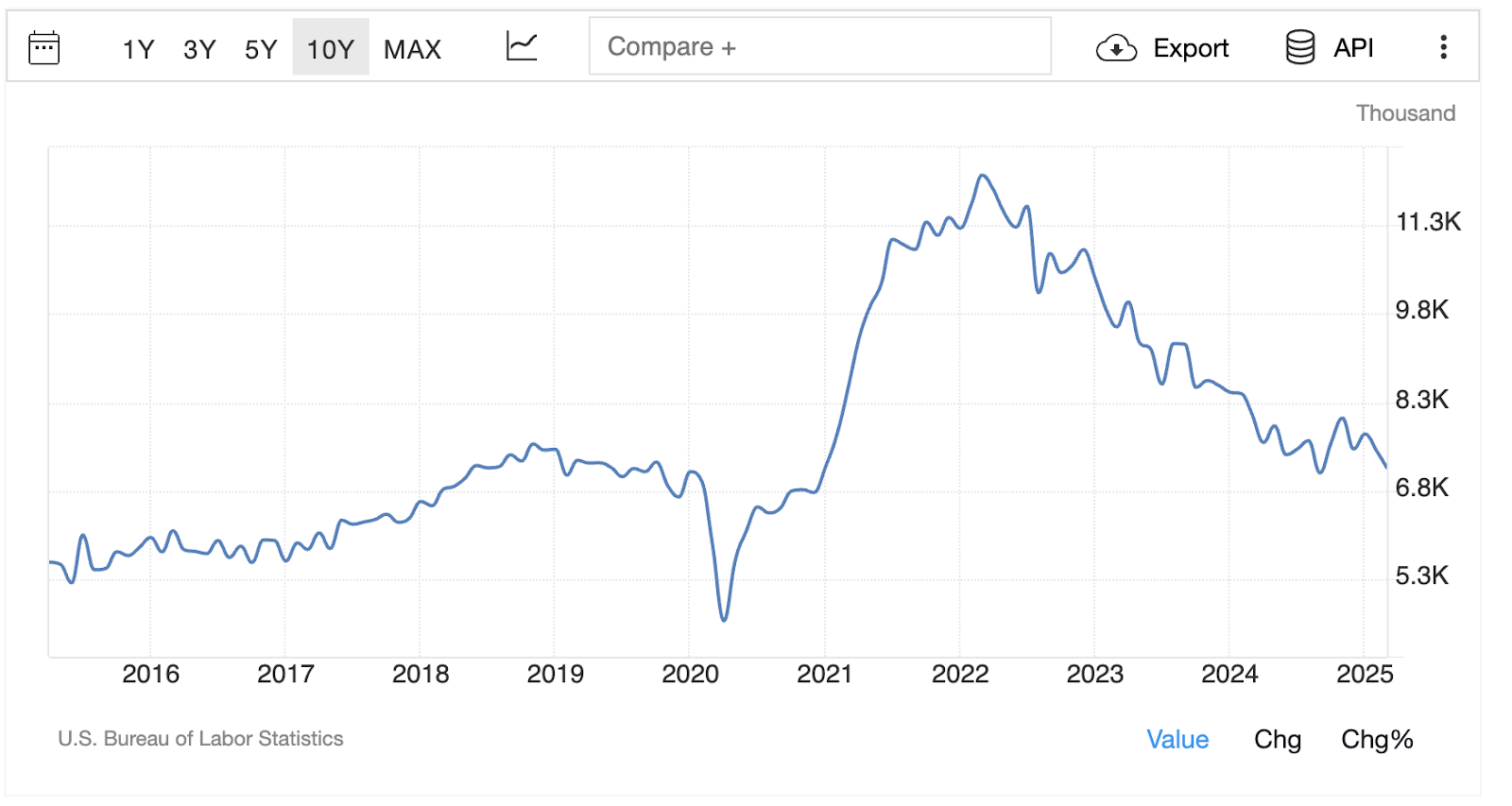

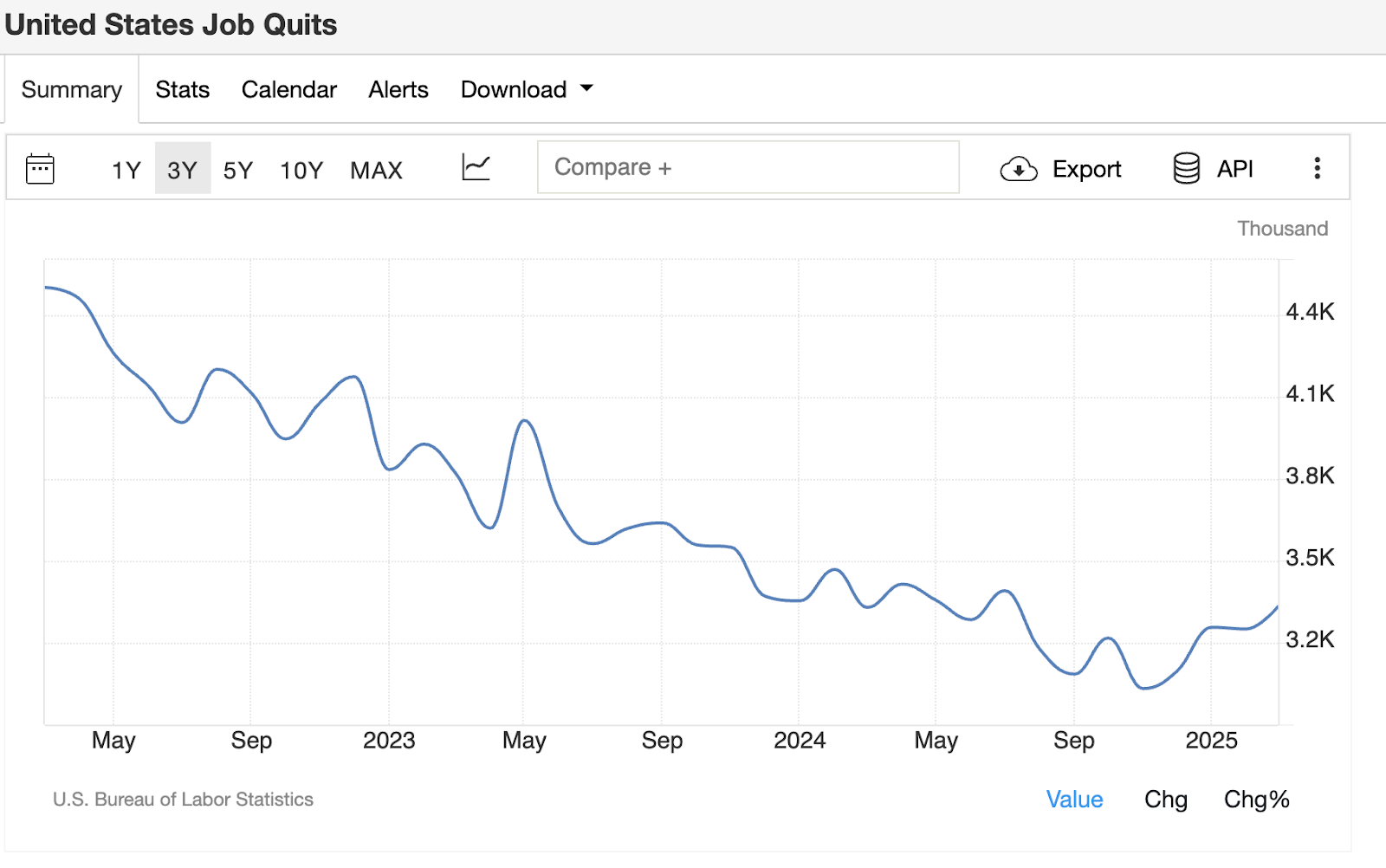

On Tuesday we acquired the Job Openings and Labor Turnover Survey (JOLTS) report. It was a blended one.

On one aspect, we noticed job openings miss to the draw back and start to roll over after a couple of months of constructive surprises:

On the opposite aspect, we noticed the quits price truly enhance, hinting at elevated confidence within the jobs market by people prepared to stop their jobs and discover one thing higher elsewhere:

It’s fairly uncommon to see these two prints diverge. I feel we’ll have to see the roles report on Friday to get a cleaner learn on the path of the labor market, which is a key driver of the Fed’s response operate.

GDP print

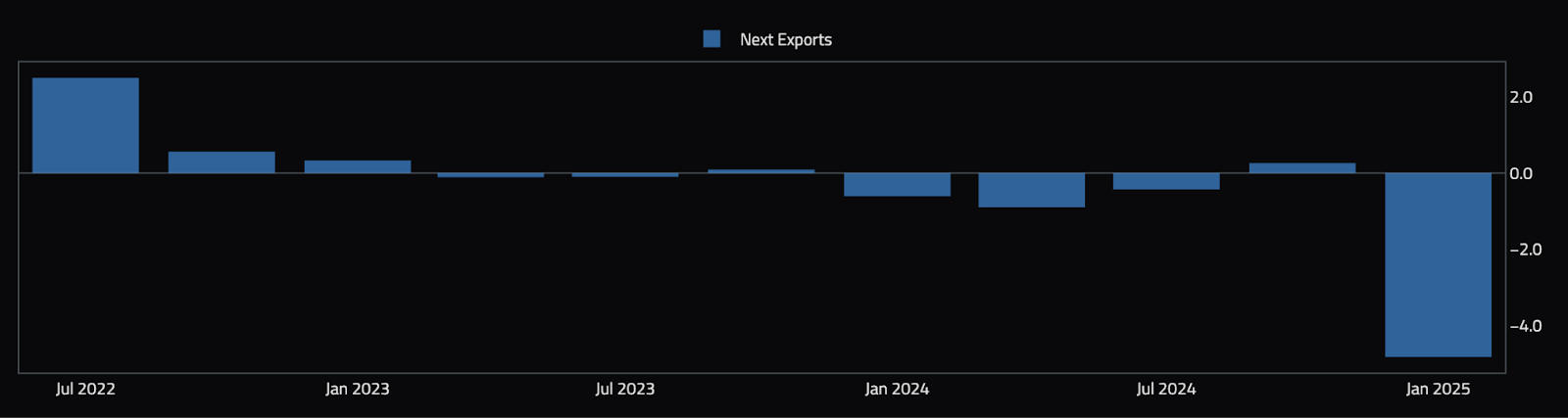

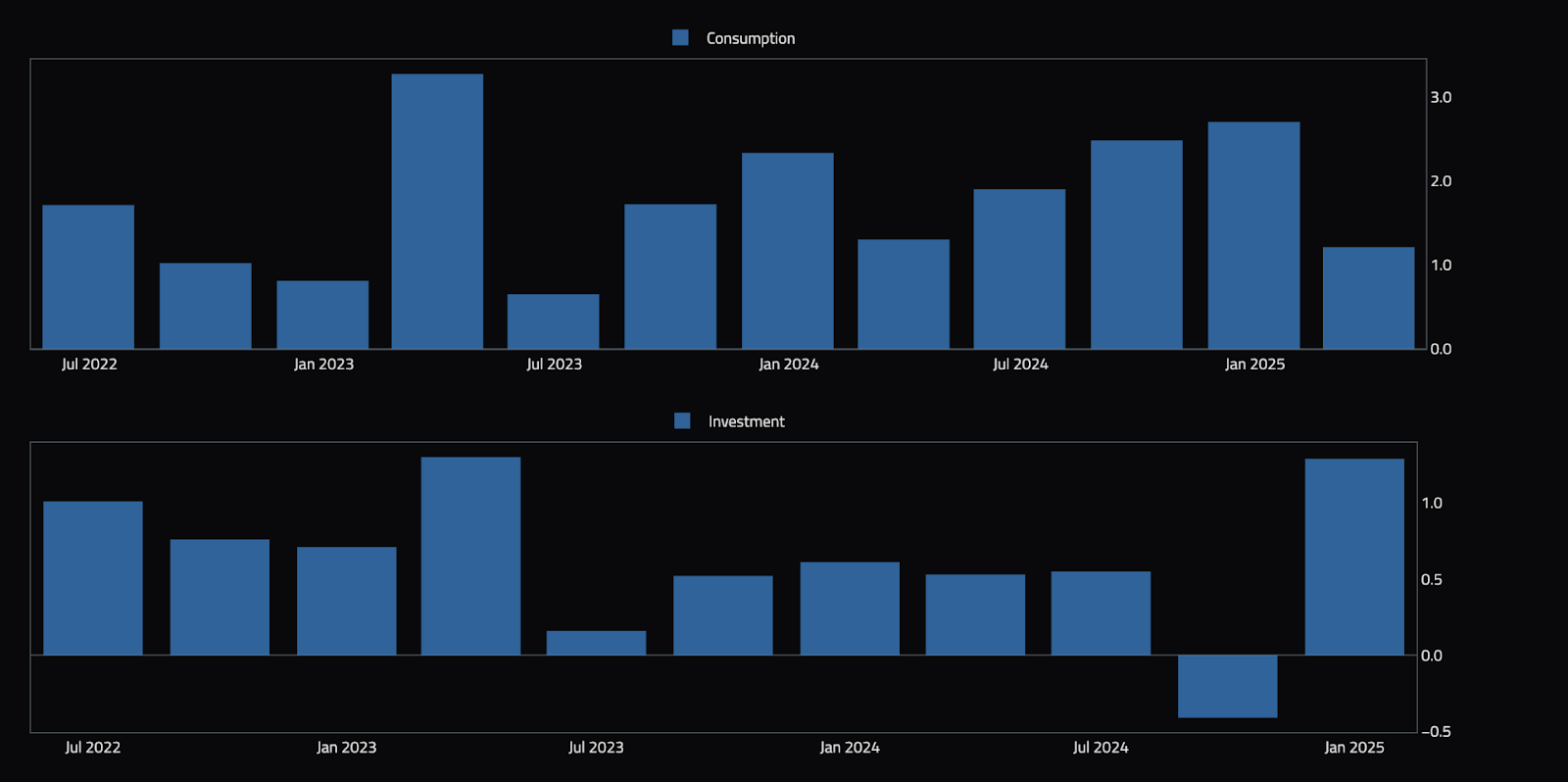

As talked about in yesterday’s publication, we acquired the primary have a look at Q1’s GDP print, which was additionally fairly blended. The topline variety of -0.3% quarter over quarter hid some fascinating insights:

The large driver was internet exports crashing decrease, primarily as a consequence of an enormous enhance in imports. That mechanically lowers GDP progress.

Nevertheless, wanting on the extra vital elements of GDP, consumption held up decently, and funding truly surged!

This hints at one thing I’ve been pondering rather a lot about lately, which is that tariffs could possibly be making a mirage within the arduous knowledge. This mirage creates the looks of a powerful financial system due to all of the tariff frontrunning that happens from each customers and companies attempting to purchase items earlier than the tariffs really start.

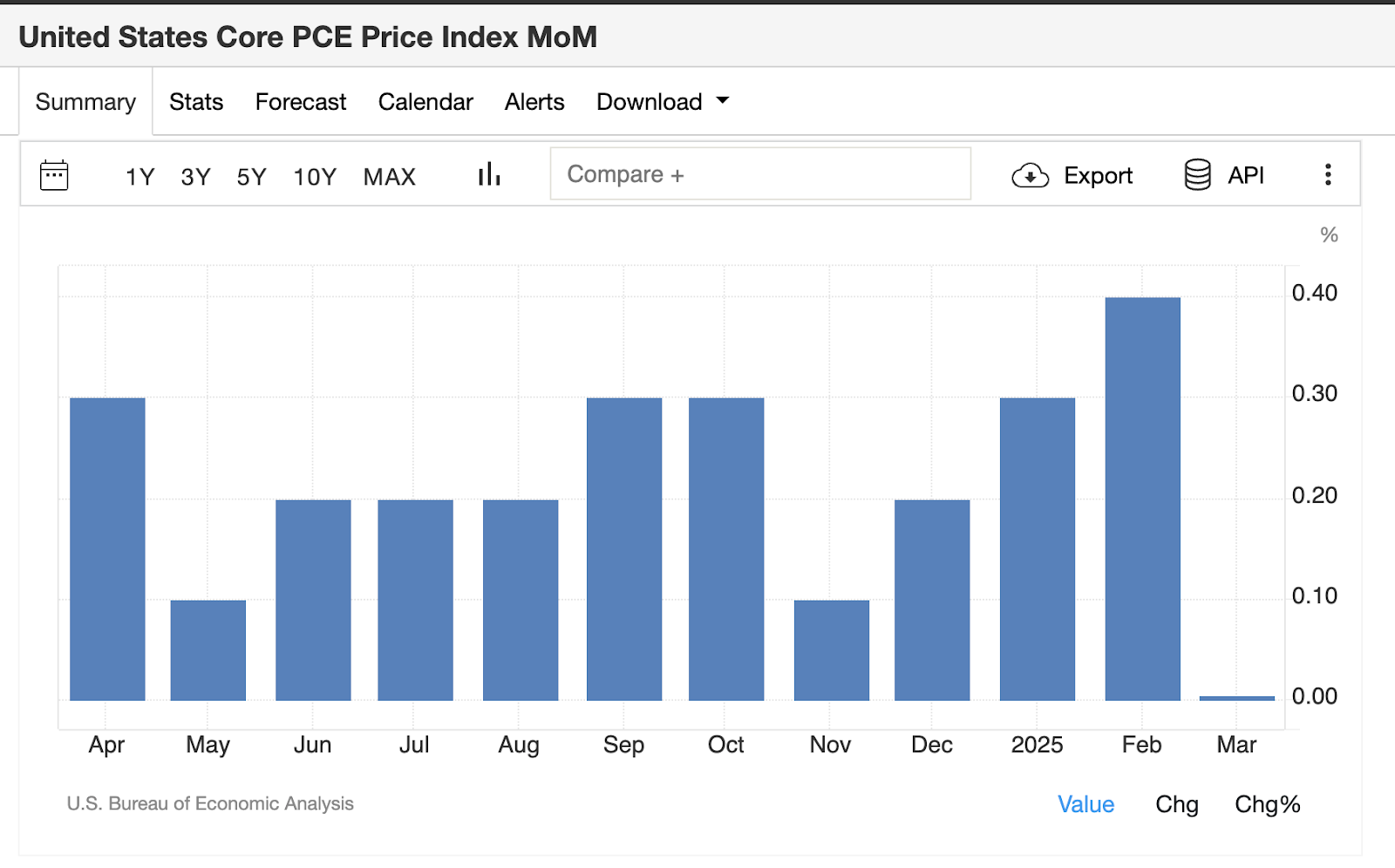

Core PCE print

We additionally obtained the Core Private Consumption Expenditures (PCE) print, which got here in at 0% month over month (vs. consensus expectations of 0.1%)!

This type of knowledge shines a lightweight on how, if it weren’t for the concern of tariff-induced inflation, inflation can be on a quick observe again to focus on and the Fed can be slicing rates of interest like mad.

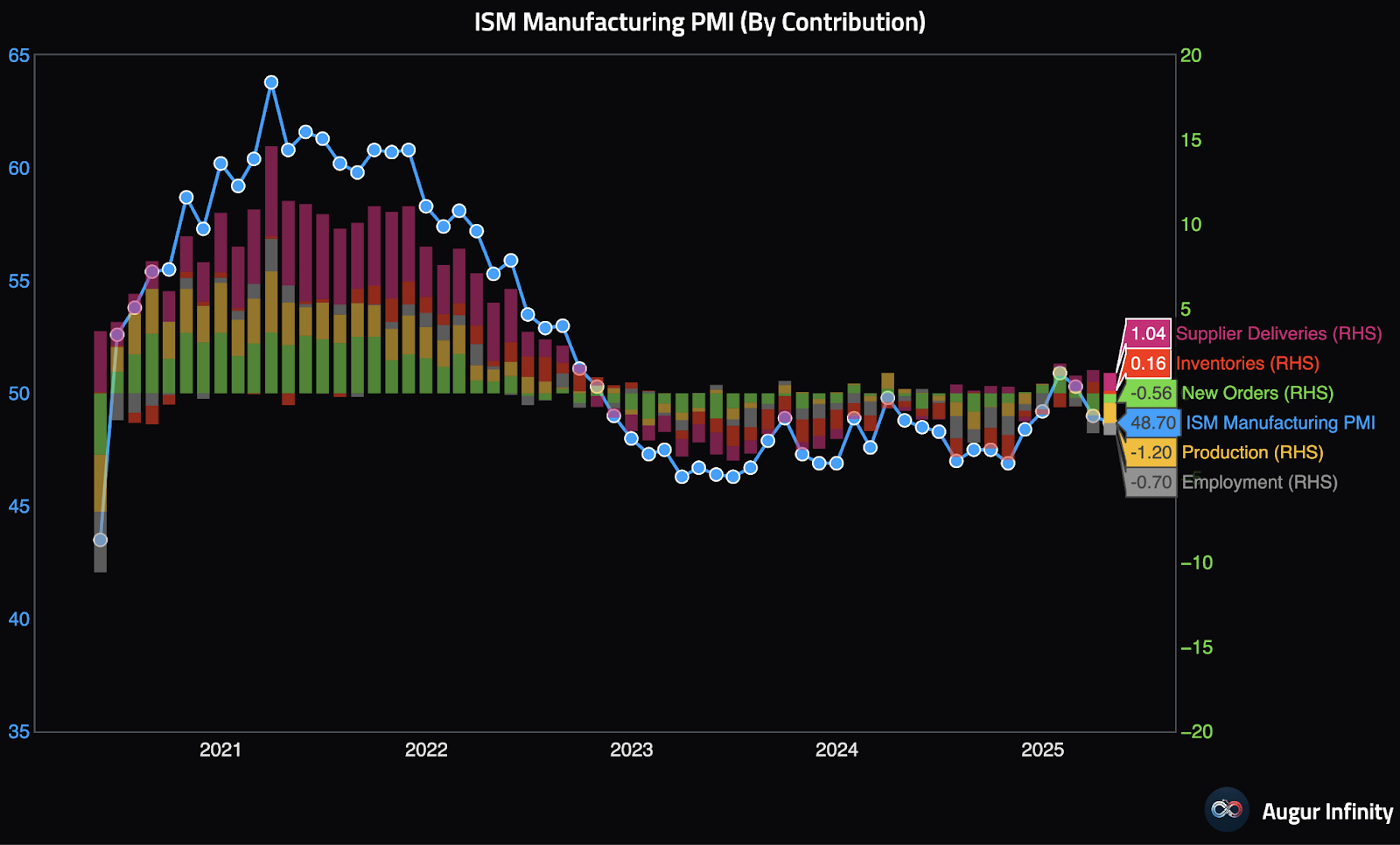

ISM survey

Lastly, in the present day noticed the ISM Manufacturing PMI survey outcomes, which offer a number one look into how the financial system is digesting the tariff conflict.