Stablecoins have lengthy been thought of the “money” of cryptocurrency markets, offering a method of buying and selling Bitcoin, transferring liquidity between exchanges, and avoiding volatility with out ever leaving the blockchain.

Now, conventional shoppers are additionally embracing stablecoins. Previously 12 months alone, stablecoin frameworks have been launched by regulators. On the similar time, stablecoin rails have been built-in by cost giants, and companies are experimenting with them for cross-border funds.

Naturally, this has raised an vital query: Are stablecoins changing banks?

Cross-border cost mechanism

To place issues in perspective, conventional cross-border funds nonetheless rely on pre-funded nostro accounts, SWIFT messaging, and correspondent banks. This makes transfers expensive, time-consuming, and opaque.

Nonetheless, now companies have a faster and cheaper solution to settle worldwide funds. Stablecoins assist full transfers in seconds and function 24/7, with out the necessity for correspondent banks or pre-funded accounts.

That profit is what’s inflicting adoption.

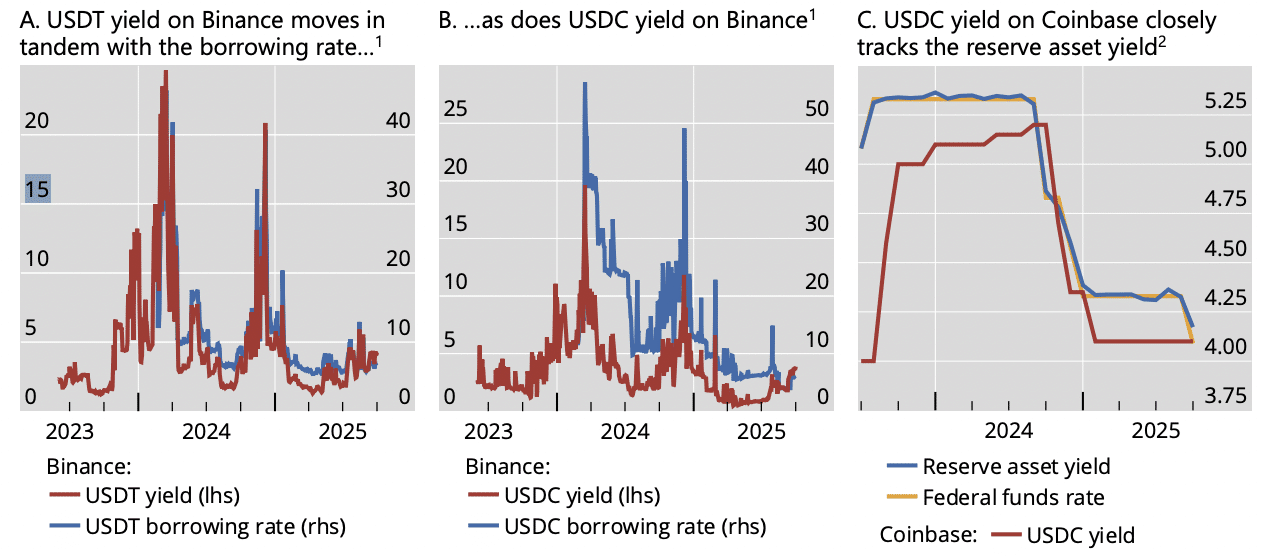

Metrics supporting the stablecoin adoption race

Mastercard, as an illustration, agreed to purchase BVNK for as much as $1.8 billion, Visa’s stablecoin settlement quantity reached a multi-billion-dollar annualized run price by late 2025, and Stripe integrated Bridge into its cost system.

This proves that banks aren’t being changed by stablecoins. Though they improve cost infrastructure, they don’t supply credit score creation, lending, or deposit insurance coverage.

In keeping with McKinsey, stablecoin funds totaled about $400 billion in 2025, whereas tokenized financial institution deposits are estimated to switch about $4 trillion yearly.

Moreover, solely 15% of each $1,000 that’s transformed into USDC or USDT returns to banks as reserves, which explains why banks are tokenizing deposits to maintain funding whereas growing blockchain effectivity.

This prompted the Financial institution of England to chill out its deliberate restrictions on stablecoins.

Blended opinion from business leaders

In an e mail despatched to AMBCrypto, Shantnoo Saxsena, CEO and founding father of Encryptus, a regulated cross-border funds infrastructure supplier, famous,

The Financial institution of England’s resolution to take away particular person possession caps and decrease reserve necessities is a welcome step ahead, however the £40bn issuance restrict suggests policymakers are nonetheless targeted on the improper danger.

Though a big portion of demand is pushed by cross-border funds, Saxsena thinks that the framework assumes stablecoins primarily compete with home financial institution deposits.

He added,

A £40bn cap on sterling stablecoins might sound beneficiant, nevertheless it successfully retains the infrastructure at pilot scale whereas greenback stablecoins issued elsewhere are already supporting actual remittance flows.

Pablo Hernández de Cos, Normal Supervisor of Financial institution for Worldwide Settlements, expressed comparable views throughout his April speech at a Financial institution of Japan seminar, the place he stated,

If extensively adopted of their present type, stablecoins would pose coverage challenges in a number of areas, starting from credit score provision to financial coverage. For policymakers, it’s key to think about how these challenges may differ from those who come up in as we speak’s two-tier banking system.

Stablecoin critics stay

Nonetheless, in a current e mail to AMBCrypto, Maksym Sakharov, CEO and co-founder of WeFi, opposed this viewpoint.

Stablecoins are placing strain on the weakest elements of cross-border infrastructure: delayed settlement, too many middleman steps, unclear prices, and sluggish reconciliation. They make the necessity for infrastructure enchancment tougher to disregard.

Moreover, regardless of his financial institution growing across the product, Jamie Dimon, JPMorgan’s CEO, has adopted a extra skeptical stance. He says he doesn’t perceive why anybody would select a stablecoin over a standard cost methodology.

Nonetheless, he additionally reiterated that JPMorgan will “be in it and studying lots” anyhow, working each its personal deposit token and third-party stablecoin rails concurrently.

The place is that this going over the following decade?

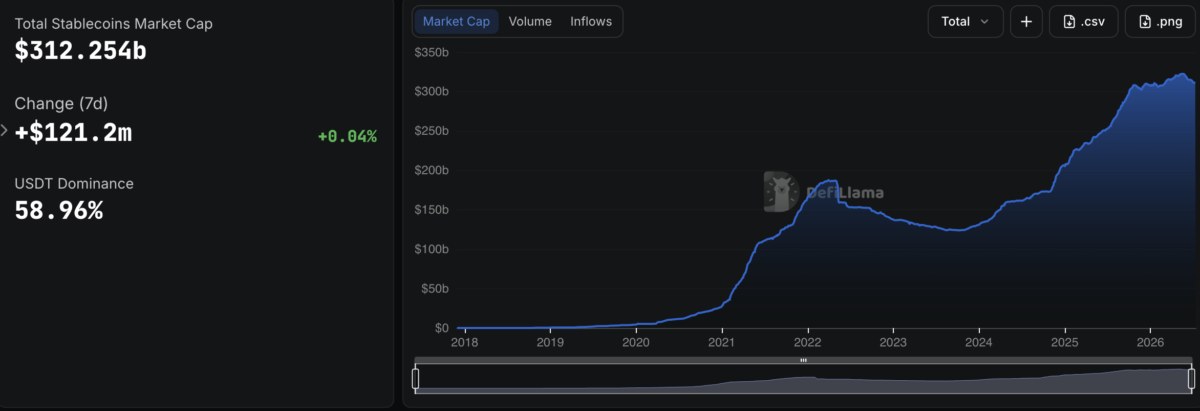

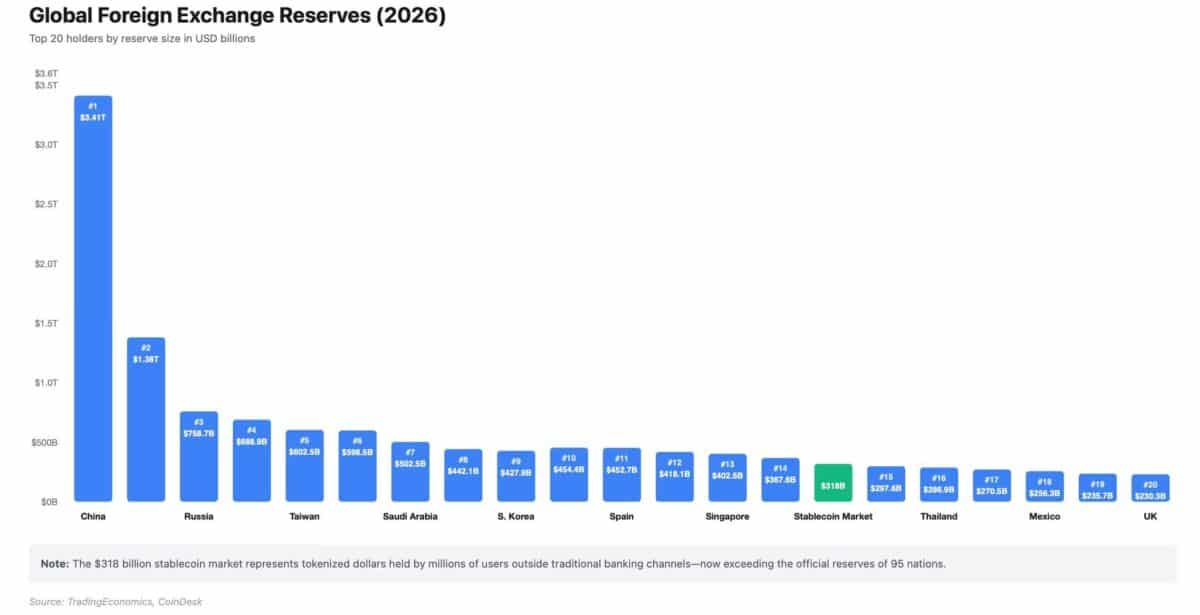

Nonetheless, the stablecoin market cap has already reached $312 billion, with Circle and Tether controlling about 85% of the provision and 99% of it being denominated in US {dollars}.

Apparently, it additionally surpasses the reserves of 95 international locations.

Right here, Sakharov added what the stablecoin market must develop additional.

Actual adoption is seen when stablecoins remedy repeated monetary issues. A freelancer getting paid by a world shopper, an organization settling with suppliers, or a enterprise managing treasury throughout markets is utilizing stablecoins for entry, velocity, and predictability.

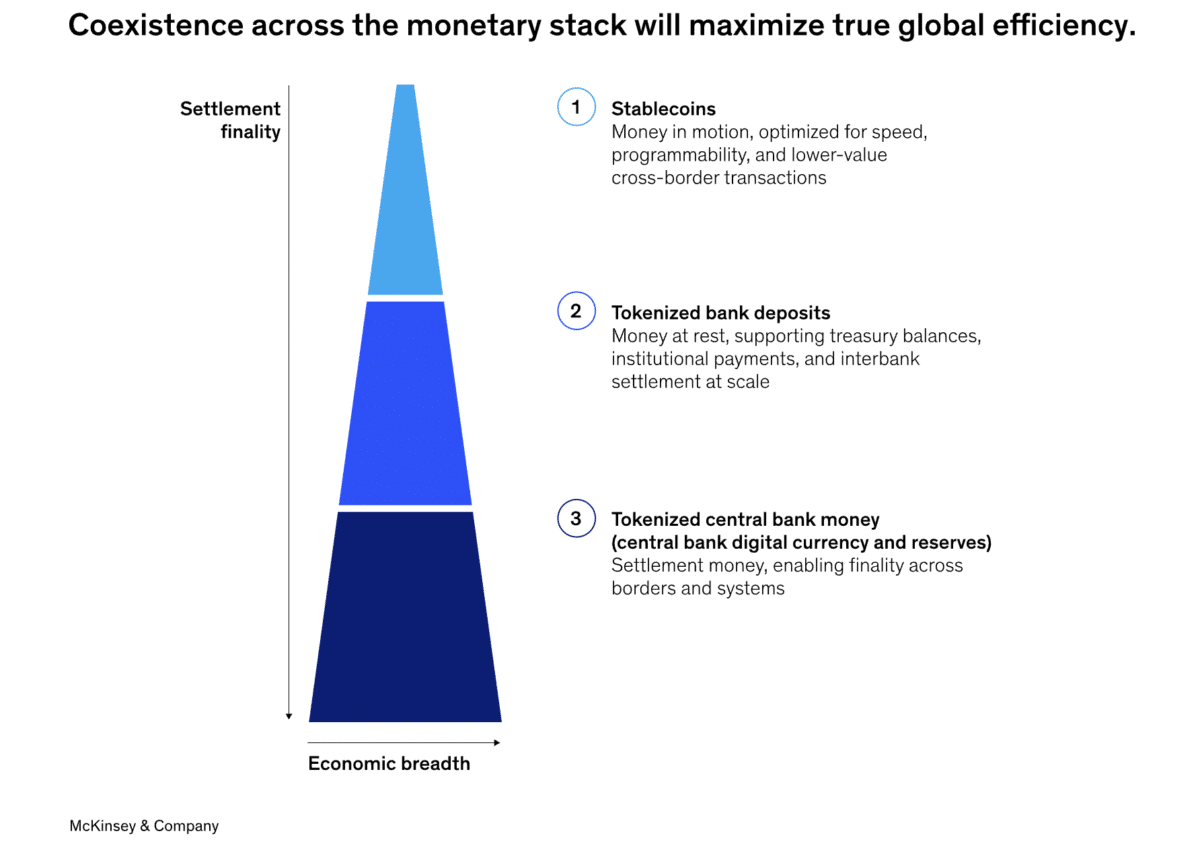

Due to this fact, it’s secure to conclude that coexistence somewhat than substitute is extra doubtless the results of the rise of the stablecoin market.

Whereas banks nonetheless supply providers like deposits, lending, and compliance, stablecoins are taking the place of the costly, sluggish cost rails that help conventional banking.

Remaining Abstract

- The stablecoin market has reached a market cap of $312 billion, with Circle and Tether controlling about 85% of the provision.

- Amidst issues about stablecoins changing banks, adoption and laws are shifting attitudes.