The period of shopping for bitcoin and calling it a treasury technique is over.

By early 2026, greater than 200 publicly listed firms maintain digital property on their stability sheets, collectively managing over $115 billion (DLA Piper, October 2025). The overall market capitalization of those firms reached roughly $150 billion by September 2025 – a virtually fourfold enhance from the yr earlier than. But a number of of those firms now commerce at reductions to the worth of the property they maintain. The market is sending a transparent sign: accumulation alone is now not sufficient.

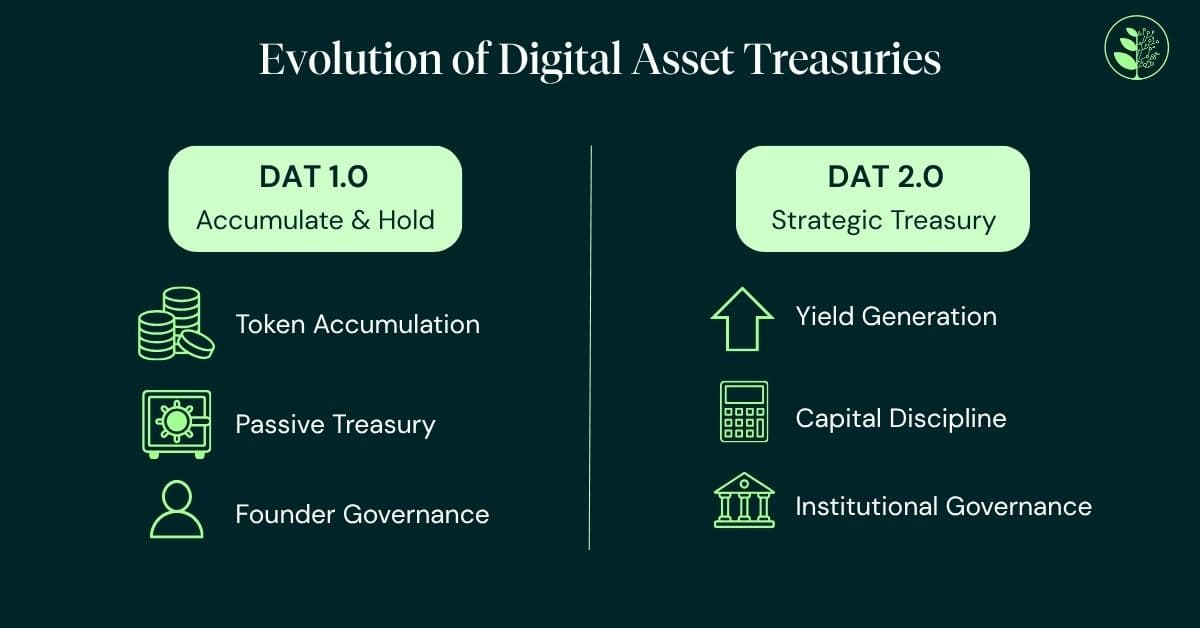

Buyers need to see capital self-discipline and financial return. Administration groups have responded with share repurchase applications and transparency metrics resembling “$BTC per share,” designed to point out the worth a treasury provides past the token value (AMINA Financial institution Analysis, 2026). The shift from passive accumulation to lively yield era – from “DAT 1.0” to “DAT 2.0”—is now the defining theme of the sector.

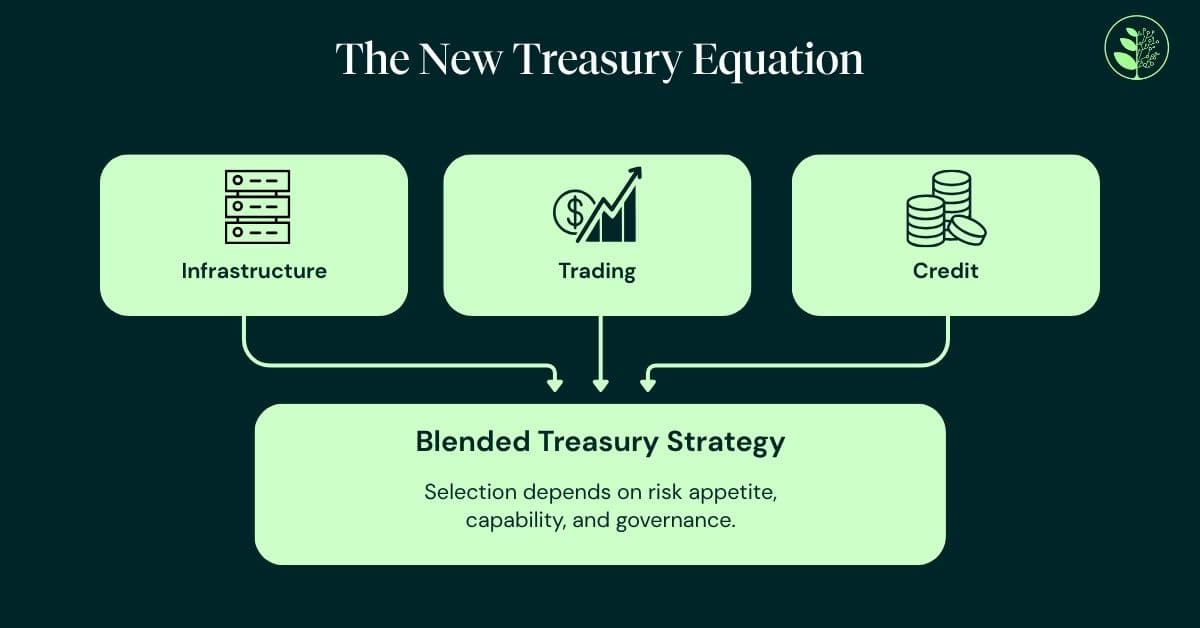

Three broad fashions are rising. Every carries a distinct danger – return profile and locations distinct calls for on governance, technical functionality and infrastructure.

Infrastructure participation and staking

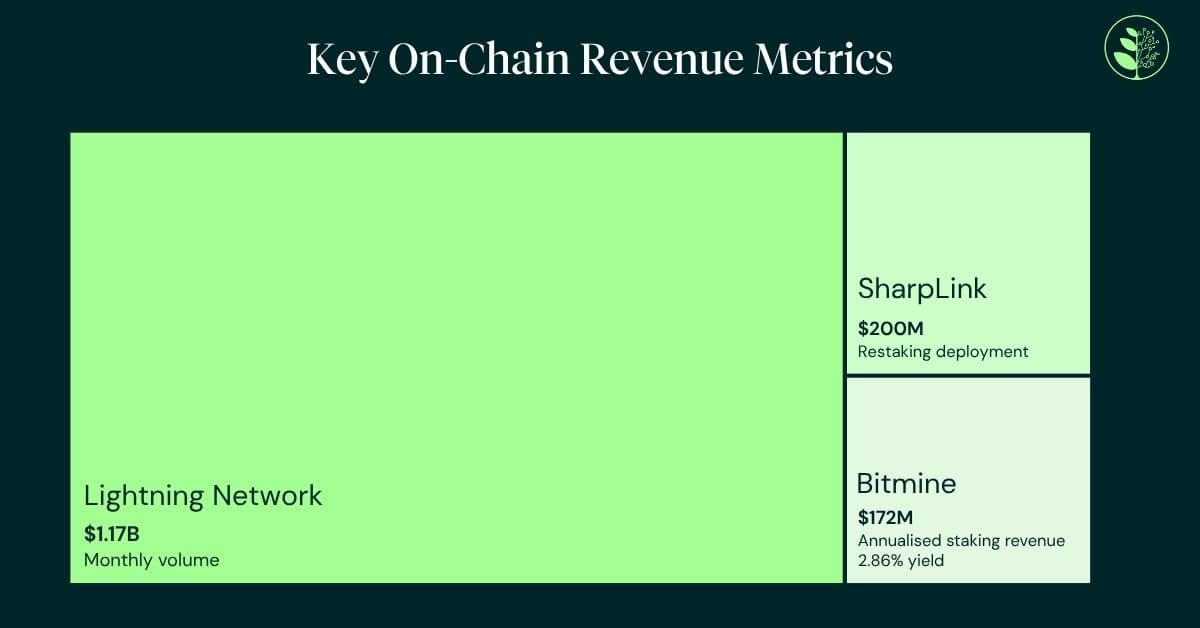

Probably the most protocol-native method includes staking tokens to help community consensus and incomes rewards in return. For bitcoin-focused treasuries, this more and more extends to the Lightning Community and different native infrastructure that generates routing and liquidity-based charges. Staking requires cautious evaluation of the technical safety and sensible contract dangers.

The numbers have grown rapidly. Bitmine Immersion Applied sciences reported over 3 million staked $ETH by early 2026, with whole holdings of $9.9 billion and annualized staking income of roughly $172 million (SEC Submitting, March 2026). Its proprietary validator community marginally outperformed the Composite Ethereum Staking Charge, demonstrating the sting that institutional-grade infrastructure can ship even in a protocol-level yield atmosphere.

SharpLink Gaming deployed $200 million in $ETH into restaking infrastructure through EigenCloud, focusing on larger yields by securing functions starting from AI workloads to identification verification (SEC Submitting, 2025). Restaking – the place already-staked $ETH is used to safe further providers, with cautious governance.

Lively buying and selling and market-driven revenue

A second set of methods leverages market construction – funding-rate arbitrage, foundation buying and selling and choices premiums. These may be efficient and infrequently market-neutral, however they demand buying and selling experience, sturdy danger controls and round the clock monitoring. The governance implications are vital: this method successfully converts a treasury perform right into a buying and selling operation. Like all buying and selling perform, it may be troublesome to seek out expert employees required to observe advanced positions and correlation dangers.

One distinguished Japanese listed firm illustrates each the potential and the complexity. Holding over 35,000 $BTC by the tip of 2025, it generated the equal of roughly $55 million in bitcoin revenue income by way of option-based methods, with working revenue progress exceeding 1,600% year-on-year. But the identical firm recorded a considerable web loss as a consequence of non-cash mark-to-market revaluations below native accounting requirements (TradingView; Kavout, 2026). For buyers, this disconnect between operational money circulate and reported earnings makes analysis materially more durable – and underscores why governance and transparency matter as a lot as headline returns.

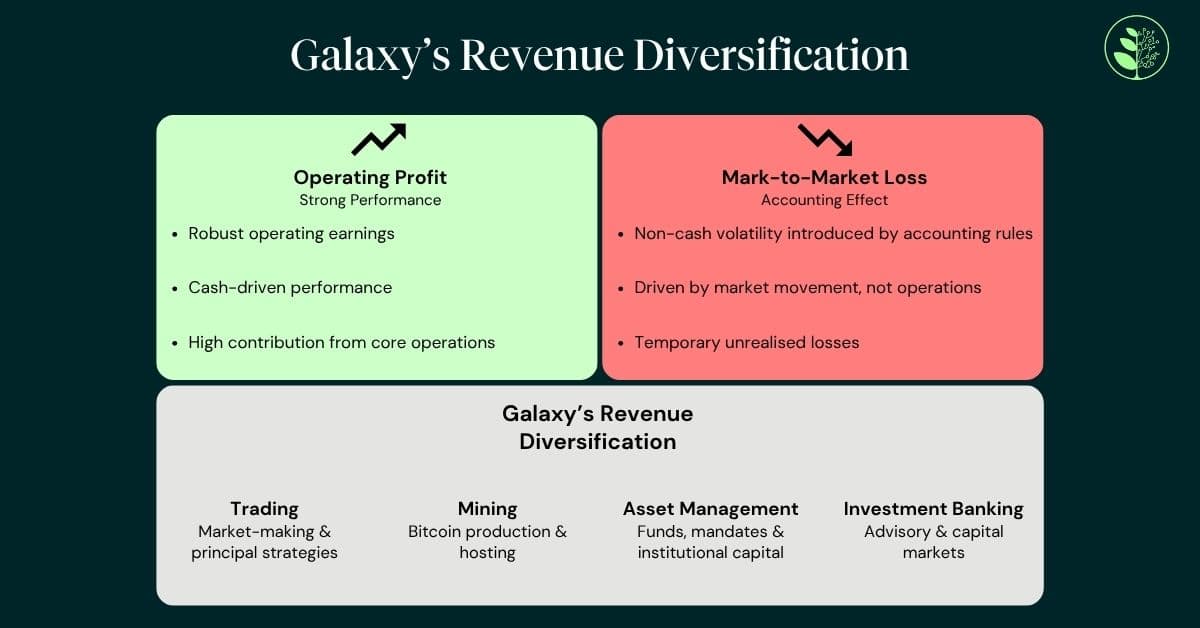

Galaxy Digital provides a contrasting hybrid mannequin, combining its personal digital asset treasury with institutional providers together with collateralized lending, strategic advisory, and infrastructure. In Q3 2025, Galaxy posted a file adjusted gross revenue of over $730 million (Mint Ventures Analysis, 2025). Notably, the agency has diversified its yield sources past pure crypto by repurposing its Helios mining facility as an AI compute campus secured by long-term contracts – a sign that essentially the most resilient treasuries could also be people who derive revenue from a number of, uncorrelated sources.

Credit score deployment and web curiosity margin

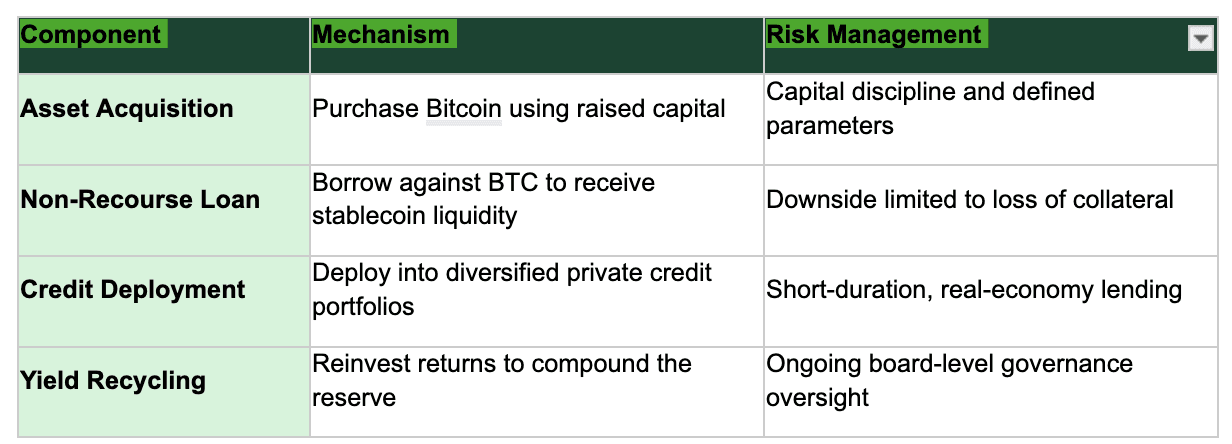

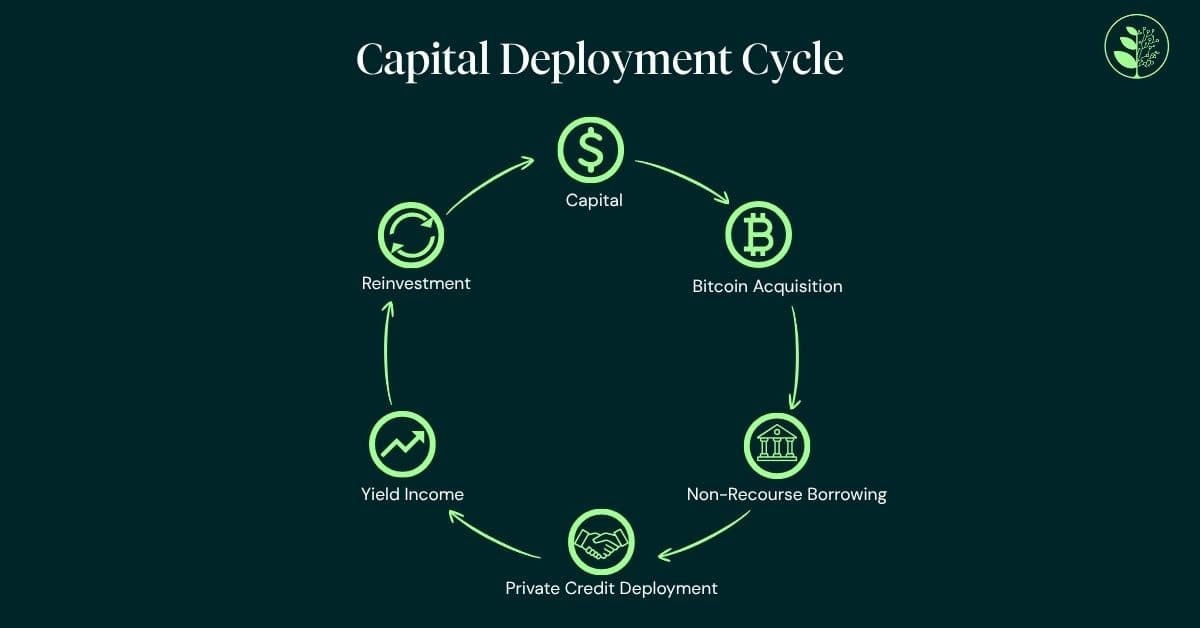

A 3rd route treats digital property as productive balance-sheet capital. The mannequin includes borrowing towards crypto holdings on a non-recourse foundation, receiving stablecoin liquidity, and deploying it into higher-yielding non-public credit score. It preserves long-term publicity to the underlying asset whereas producing recurring curiosity revenue from short-duration, real-economy lending. Specifically, this technique calls for experience in yield, credit score danger and stuck revenue.

The mechanics draw straight from conventional banking: liquidity administration, underwriting, governance and managed leverage. Below the sort of mannequin, an organization acquires bitcoin, borrows towards these holdings on a non-recourse foundation—which means the draw back is proscribed to the collateral—and deploys the proceeds into diversified non-public credit score portfolios supporting real-economy lending. If bitcoin appreciates, the corporate retains the upside after repaying the mortgage, combining potential capital beneficial properties with recurring curiosity revenue.

For credit score deployment fashions to work credibly, they have to be grounded in operational monetary infrastructure quite than constructed from scratch. The method is only when it extends from an present platform with actual lending relationships and established shopper accounts. In our view at Greenage, that is additionally an space the place governance and due diligence frameworks are significantly necessary, provided that capital is being deployed into third-party credit score alternatives that have to be assessed on a counterparty-by-counterparty foundation.

The success of this mannequin can be tied to the maturation of stablecoins as institutional infrastructure. By 2026, stablecoins underpin cross-border funds, real-time settlement and T+0 clearing (same-day settlement) for enterprises (Foley & Lardner, January 2026). Coinbase Institutional initiatives whole stablecoin market capitalization may attain $1.2 trillion by 2028 (Coinbase Institutional, August 2025). For credit score deployment methods, stablecoins present a sound medium for capital deployment in lending markets.

The brand new measure of maturity

Latest market situations have bolstered a easy fact: value appreciation alone is just not a treasury technique. The rising vary of yield options displays a sector studying from its personal historical past—sustainable revenue era makes digital property extra productive parts of a company stability sheet.

No single mannequin is definitive. The best treasuries will mix approaches relying on danger urge for food, operational functionality and governance construction. However the path of journey is evident. Passive holding is now not ample to justify digital property’ place on the stability sheet. Yield is turning into the central measure of treasury maturity –and the core think about how the market values firms with digital asset publicity.

The winners on this subsequent part is not going to be the biggest holders. They would be the most disciplined operators.

Essential Discover:

This text has been ready by Greengage & Co. Restricted for informational and thought management functions solely. It’s meant solely to be used by companies, skilled counterparties and institutional market individuals and isn’t directed at retail customers. It doesn’t represent monetary recommendation, funding recommendation, a monetary promotion, or a advice or inducement to purchase, promote, or maintain any asset, safety, or monetary instrument.

Digital property are topic to vital value volatility and regulatory change. Previous efficiency is just not indicative of future outcomes. All investments carry danger, together with the potential lack of capital. Ahead-looking statements and market projections referenced herein are sourced from third-party analysis and don’t signify the views or predictions of Greengage & Co. Restricted.

Greengage & Co. Restricted is just not approved or regulated by the Monetary Conduct Authority for funding enterprise. Greengage acts solely as an introducer to impartial third-party service suppliers and doesn’t organize investments, present lending, custody, or funding administration providers.

Readers ought to search impartial skilled recommendation earlier than making any funding determination.