It is a phase from the 0xResearch e-newsletter. To learn full editions, subscribe.

ETH is buying and selling at ~$1,600 in the present day.

Can ETH pump once more? Wen moon?

Attending to the guts of this easy query requires an inevitable detour into the boring, technical weeds of information availability (DA).

The ELI5 clarification of information availability is storage charges, or bandwidth useful resource. All chains – L1s and L2s – want them to function, however their main provider is the L1.

Right here’s the tough practice of thought:

- What’s the destiny of ETH as an asset?

- That will depend on how properly Ethereum can generate charges.

- Ethereum generates charges in three main methods: execution, MEV, and information availability.

- Execution charges (aka congestion charges) have largely been given as much as L2s, as per the intent of the rollup-centric roadmap.

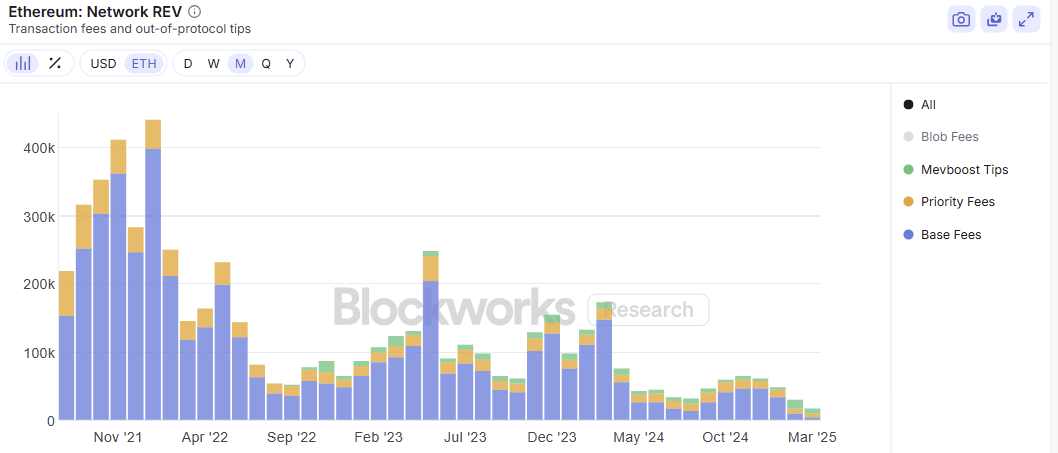

- MEV charges are compressing attributable to higher analysis. Increasingly wallets and apps are discovering higher methods to retain MEV and return them to customers. The beneath chart of Ethereum’s REV (actual financial worth), excluding blob charges, is a tough proxy for the way Ethereum’s MEV has been trending down over time.

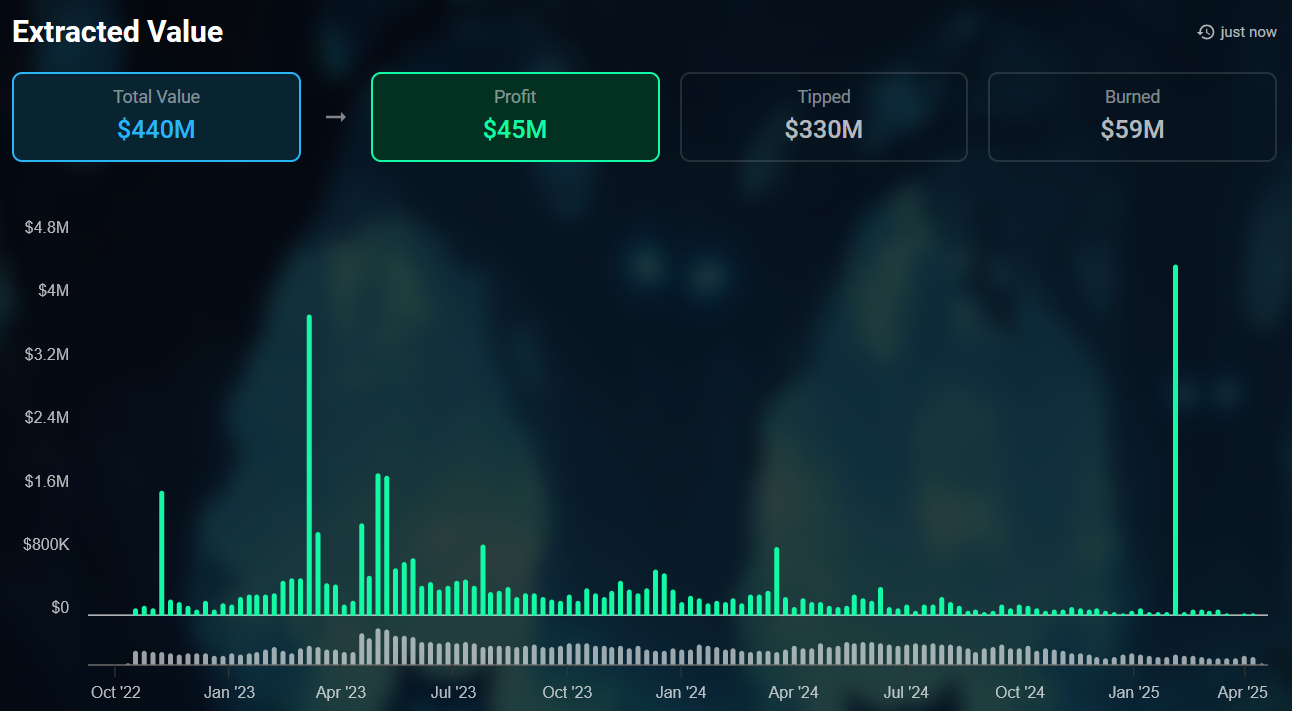

One other method to have a look at the downtrend of MEV is the diminishing extracted worth of sandwich assaults. That is largely attributable to an growing quantity of Ethereum non-public transaction orderflow that isn’t going via the general public mempool.

Supply: Libmev

- As extra rollups launch, and since each chain wants DA, DA charges stay ETH’s final bastion of worth accrual.

So we’ve established that information availability charges are important to Ethereum’s success.

That isn’t simply my opinion; it’s the express place of main Ethereum researchers like Justin Drake. As he places it within the newest Ethereum Basis Reddit AMA, DA is “the one sustainable supply of flows for L1s,” not for execution or MEV charges.

(I notice it is a simplification. There are efforts to scale the L1 and to draw institutional capital to the L1, however put that apart for now.)

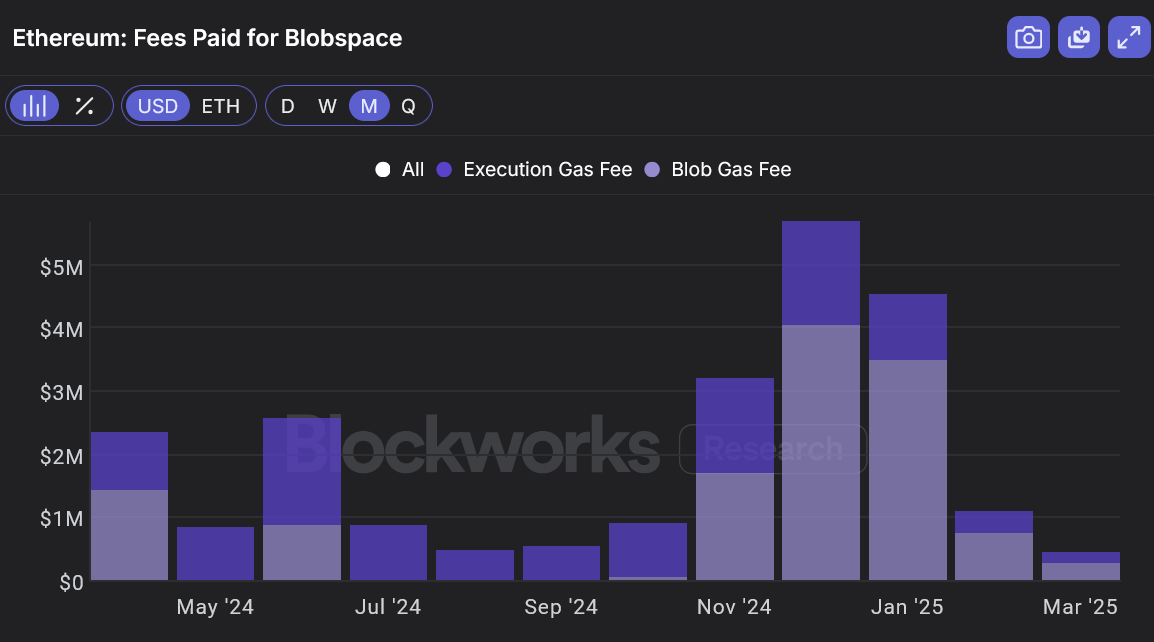

Now, let’s take a look at how a lot Ethereum makes from DA in the present day.

Sadly, not a lot. For the reason that inception of EIP-4844 in March 2024, Ethereum has generated a complete of $26m in charges.

Reaching that payment stage is a operate of each demand (rollups) and provide (Ethereum L1 DA capability).

Let’s assume Ethereum had ample consumer demand in the present day. Even then, Ethereum lacks the availability.

EIP-4844 launched blobs to Ethereum’s DA capability in March 2024. Blob capability is about 384 KB per slot, or roughly 32 KB/s.

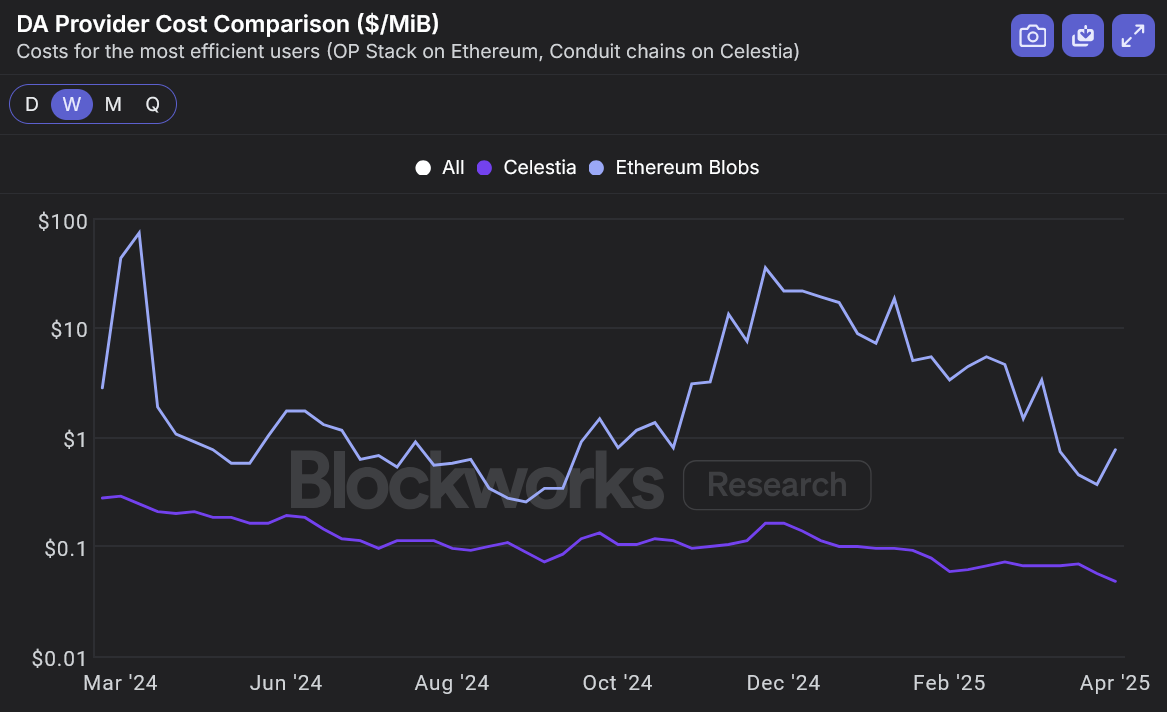

For context, alternative-DA layers like Celestia have 8 MB blocks in the present day which might be about 182% bigger. (Celestia is gearing up for 128 MB blocks.)

Sure, blob capability is increasing, nevertheless it’s gradual. DA capability is about to broaden from 3 blobs to six blobs within the Pectra laborious fork subsequent month. The eventual plan is to broaden blob capability to 48-72 within the subsequent Fusaka laborious fork, however who is aware of when that’s going to occur.

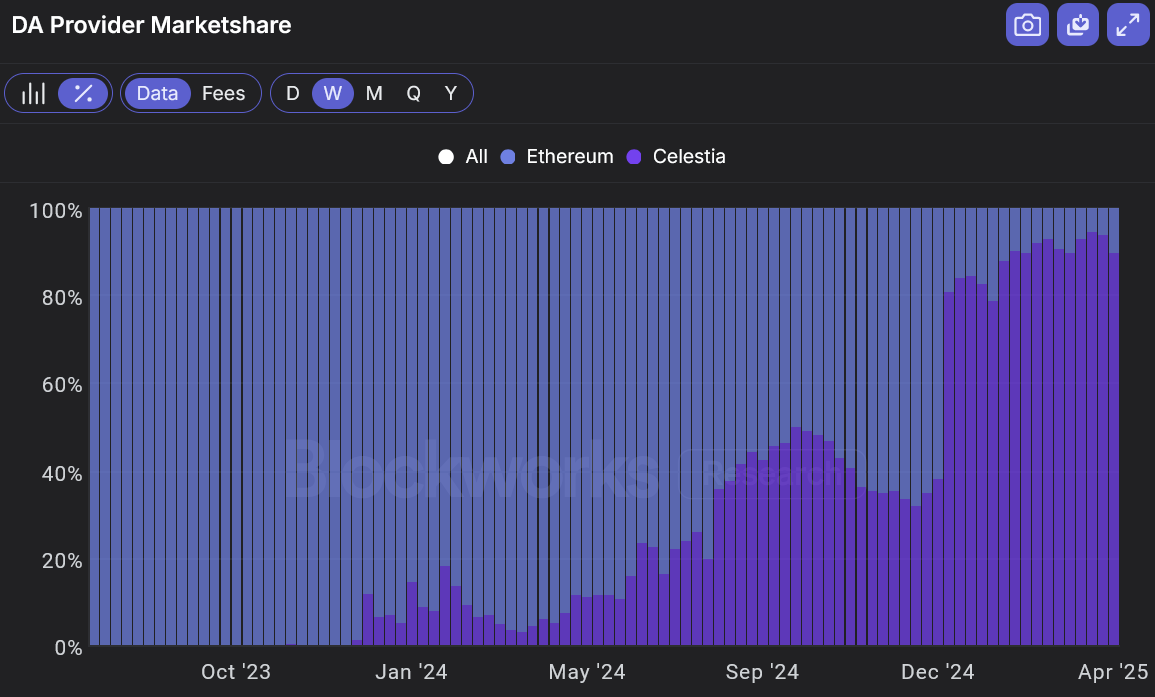

Now, let’s take a look at the DA market.

Extra unhealthy information. It’s a aggressive market. There’s Celestia, EigenDA and Avail.