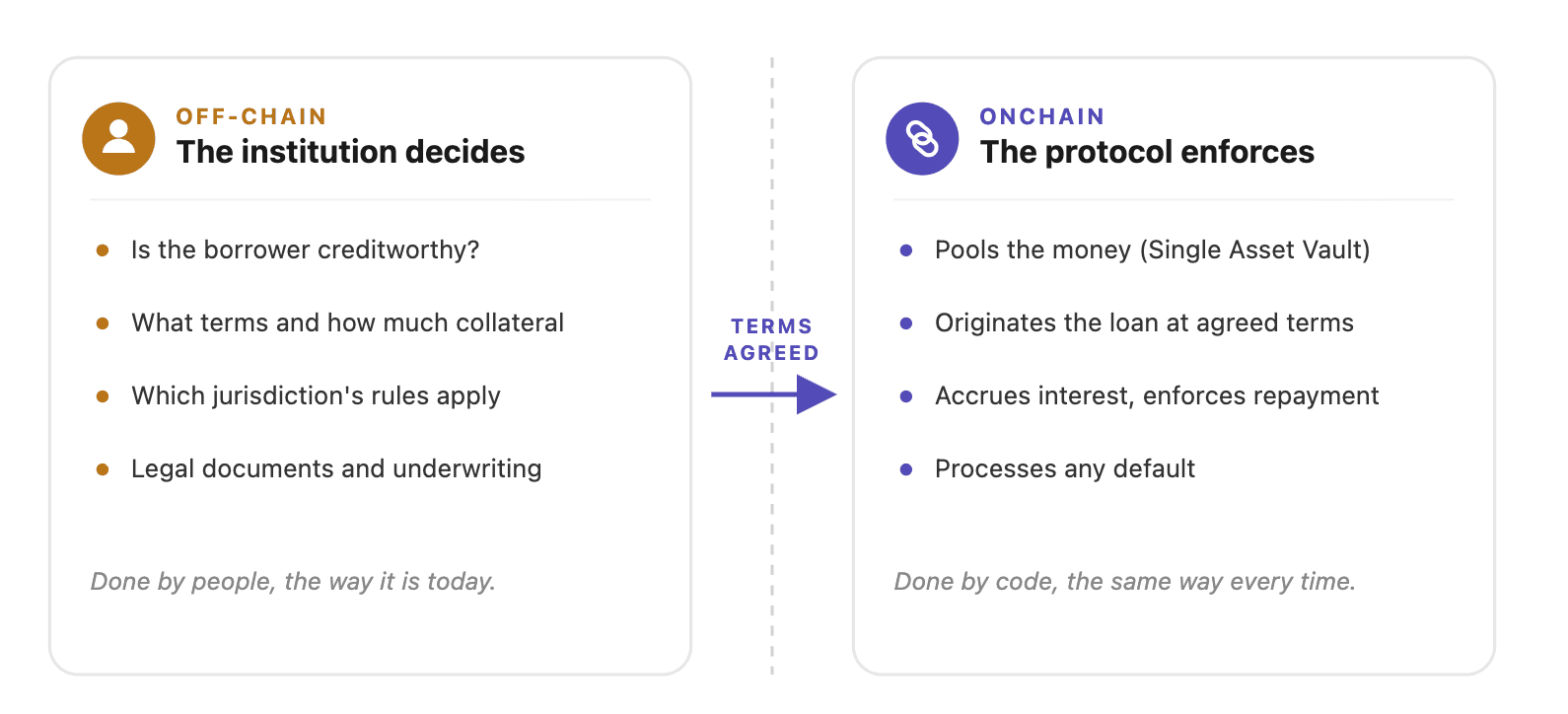

The protocol has two elements. A Single Asset Vault swimming pools a single asset, and the lending layer turns that pooled cash into loans with set phrases. Each are nonetheless proposals, outlined in technical drafts often known as XLS-65 and XLS-66, and stay topic to approval by the validators who run the community. The options can be found to check on a growth community however aren’t reside.

The use Ripple leads with is short-term financing. A fee firm holding reserves in $RLUSD, its US dollar-pegged stablecoin, may want money to fund outgoing funds earlier than a cross-border settlement clears two days later.

As an alternative of drawing on a financial institution credit score line or promoting property, it may borrow in opposition to the incoming settlement by an accredited pool, with compensation enforced routinely.

That is separate from $XRP, the token the community is greatest identified for, and from $RLUSD, which is without doubt one of the property such a system may lend in opposition to. It’s infrastructure aimed toward establishments reasonably than a product retail customers would contact instantly.

Ripple can also be strolling right into a crowded discipline, nonetheless. Onchain lending already runs at scale by protocols like Aave, Compound, Maple and Clearpool, which collectively maintain billions in deposits.

Nevertheless, Ripple says that these programs had been constructed round crypto-native governance, the place a protocol can change its threat guidelines by group votes, which it says establishments can’t underwrite prematurely. Its counter is to repair the lending mechanics on the community’s base layer so the habits doesn’t shift beneath a lender, whereas maintaining the community public reasonably than walling it off to a closed group as some permissioned programs do.