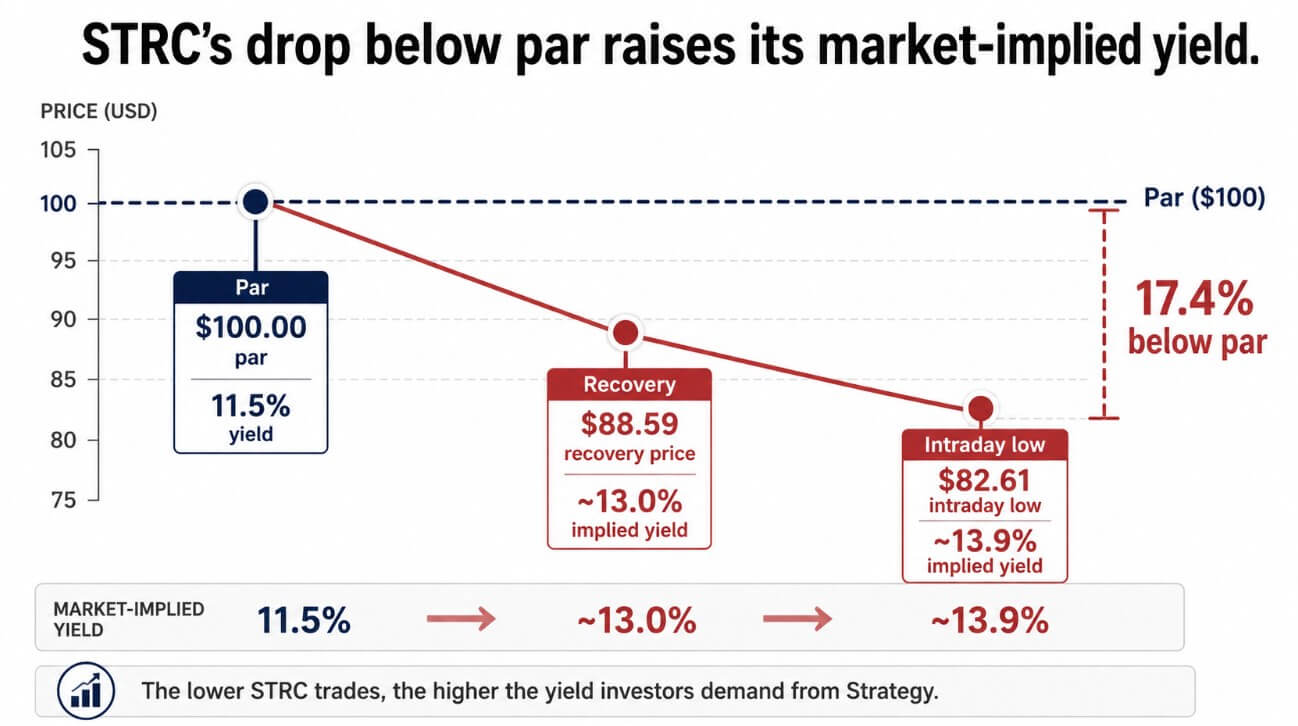

STRC, Technique’s perpetual most popular inventory, traded as little as $82.61 on June 18 earlier than recovering to $88.59, placing the safety almost 17% under its $100 acknowledged quantity on the intraday low.

MSTR fell 3.4% to $112.53 throughout the identical session, whereas Bitcoin traded close to $62,730, down about 2.5%.

Technique designed STRC to hover round $100 by month-to-month dividend-rate changes, presently set at 11.50% annualized, payable semi-monthly in money.

At $88.59, that 11.5% coupon implies an efficient yield of roughly 13.0%, and the disconnect between the acknowledged charge and market demand exhibits how far confidence has slipped.

With roughly $10.5 billion of STRC notional excellent, an 11.5% annual charge implies roughly $1.21 billion in STRC-only dividend prices.

If the market retains pricing under par and Technique responds by elevating the speed to 14%, the price would rise to about $1.47 billion yearly, which is a dynamic that critics have been warning about for months.

What the criticism acquired proper

The Ponzi-like characterization of STRC has circulated extensively, with Peter Schiff calling it “the obvious Ponzi” and arguing that new capital fund funds go to present holders.

Technique’s filings describe STRC as perpetual most popular fairness with disclosed dangers and discretionary dividend mechanics. The corporate has no authorized obligation to take care of STRC close to $100, and its personal prospectus warns that elevating the dividend when STRC trades under par might fail to revive the worth.

Tyler Wellener, CSO at Tyr Capital, commented on the structural downside in a word:

“The capital construction has turn into extra advanced over the past yr, and the market is nervous about their capacity to maintain everybody joyful and fulfill the obligations.”

He added that STRC is a confidence recreation in administration, as it’s not actually backed or collateralized by Bitcoin. A 2.5% Bitcoin drawdown produced a 17% intraday swing in STRC as a result of the instrument’s stability relies on steady confidence in Saylor’s capital allocation.

Ryan Haczynski, head of protocol partnerships at GlobalStake, identifies a second accelerant. On-chain STRC derivatives and tokenized share merchandise had been buying and tokenizing shares, whereas bigger members had constructed massive brief positions.

As STRC spent months buying and selling near par, buyers handled it as a low-volatility carry and added leverage to reinforce yield.

When the worth slipped under key ranges, margin calls triggered a cascade of liquidations, amplifying the transfer.

Haczynski additionally notes that Saylor lately acknowledged ChatGPT performed a job in creating the STRC construction, a element that compounded promoting strain because the clip circulated alongside the worth decline.

Why promoting Bitcoin doesn’t repair this

Technique disclosed that it offered 32 BTC between Might 26 and Might 31 for $2.5 million, with the proceeds anticipated to fund most popular inventory distributions.

The corporate subsequently purchased 1,550 BTC for $101.3 million, bringing complete holdings to 845,256 BTC as of June 7 and elevating its US greenback reserve to $1 billion.

The 32 BTC sale was financially negligible, roughly 482 instances smaller than one yr of STRC-only dividends on the present charge, however it cracked the narrative that Saylor would by no means promote.

Wellener addressed the BTC sale query:

“Promoting BTC will weaken their steadiness sheet and spook the market as massive BTC holders might look to promote their BTC to de-risk, and customary fairness holders might notice they’re higher off holding BTC immediately or shopping for one of many ETFs.”

MSTR shareholders purchased the inventory to build up Bitcoin per share, whereas STRC holders purchased it for yield. Promoting Bitcoin to fund dividends appeases one constituency whereas alarming the opposite, and does nothing to handle whether or not Technique can generate yield with out constantly refinancing by new capital.

Haczynski mentioned that Technique’s seemingly subsequent transfer entails some mixture of a better dividend charge, opportunistic buybacks of discounted STRC shares, or further capital raises utilizing MSTR or conventional debt.

Elevating the dividend will increase the annual burden and offers ammunition to critics who warn of a suggestions loop. MSTR issuance preserves the Bitcoin stack however dilutes widespread shareholders and reduces BTC-per-share accretion, the core metric that MSTR patrons care about.

A buyback can be the strongest confidence sign, since repurchasing STRC at a steep low cost and reissuing it nearer to par could possibly be accretive to MSTR shareholders, however it consumes money that might in any other case fund dividends or purchase Bitcoin.

| Rescue choice | The way it helps STRC | Tradeoff | Who takes the ache |

|---|---|---|---|

| Elevate STRC dividend | Narrows the hole between acknowledged payout and market yield | Raises annual money burden and feeds feedback-loop considerations | Technique steadiness sheet |

| Promote Bitcoin | Gives money for most popular distributions | Weakens the “by no means promote” accumulation narrative | MSTR holders / BTC bulls |

| Challenge MSTR inventory | Preserves Bitcoin holdings whereas elevating money | Dilutes widespread shareholders and BTC-per-share accretion | MSTR holders |

| Purchase again STRC | Indicators confidence and captures low cost to par | Makes use of money that might fund dividends or BTC purchases | Technique liquidity |

| Let STRC reprice | Avoids throwing capital at market help | Admits STRC might commerce like distressed Bitcoin credit score | STRC holders / repute |

Wellener shared what a reputable repair requires:

“Technique’s capacity to proper the ship will come all the way down to if they’ll persuade the market they’ll enhance BTC per share with out counting on fairness issuance or monetary engineering.”

He added that transferring past buy-and-hold to make use of derivatives for yield era, as commodity companies have achieved for 20 years, might present a path to actual yield that doesn’t depend upon capital-market entry or Bitcoin worth appreciation.

What the market costs subsequent

If Technique pronounces buybacks, raises its US greenback reserve, or outlines a reputable derivatives-based yield technique, STRC can get well towards the $95-$100 vary.

Haczynski described the transfer as a liquidity unwind: the corporate held $1 billion in USD reserves as of June 7 towards a quarterly STRC dividend obligation of roughly one-quarter of $1.21 billion.

A well-structured buyback at present costs can be accretive and would reveal that the $100 par goal is greater than a advertising and marketing declare.

If STRC holds under $90 and the market begins pricing a 14% efficient yield as the brand new baseline, the suggestions loop the critics described turns into self-reinforcing.

Dividend hikes enhance the money burden with out restoring par, MSTR issuance to fund these hikes dilutes widespread holders, and Bitcoin gross sales to cowl shortfalls undermine the buildup thesis.

The instrument reprices as distressed Bitcoin credit score, with completely different investor expectations, completely different purchaser bases, and a a lot larger bar for confidence restoration.

| State of affairs | Set off | STRC impression | Broader market implication |

|---|---|---|---|

| Confidence restore | Buybacks, larger USD reserve, credible yield technique | STRC strikes again towards $95–$100 | Market treats the plunge as a liquidity occasion |

| Managed repricing | STRC stabilizes under par however dividends stay credible | STRC trades as high-yield Bitcoin-linked most popular | Traders demand larger compensation however keep away from panic |

| Yield spiral | STRC stays under $90 and Technique raises payout repeatedly | Money burden rises with out restoring par | Criticism of the construction intensifies |

| BTC-sale backlash | Technique sells extra Bitcoin to fund distributions | STRC might get fee help, however MSTR weakens | Accumulation narrative breaks additional |

| Sector repricing | Traders query Bitcoin-based yield merchandise broadly | STRC turns into the cautionary case | Future BTC treasury merchandise face larger collateral and yield scrutiny |

The broader implication extends past Technique, as Bitcoin-based yield merchandise are being stress-tested at scale as credit score devices for the primary time.

If STRC can not maintain par with an 11.5% dividend, a $10.4 billion notional base, and 845,256 Bitcoin on the steadiness sheet, the subsequent era of Bitcoin treasury merchandise will face tougher questions on collateral buildings, yield sustainability, and what it means to supply yield backed by a non-yielding asset.