On Mar. 31, Moody’s assigned provisional Ba2 rankings to as much as $100 million in taxable income bonds for the Waverose Finance Challenge. The bonds are secured by a mortgage to NH CleanSpark Borrower Belief 2026-1, with Bitcoin (BTC) because the pledged collateral.

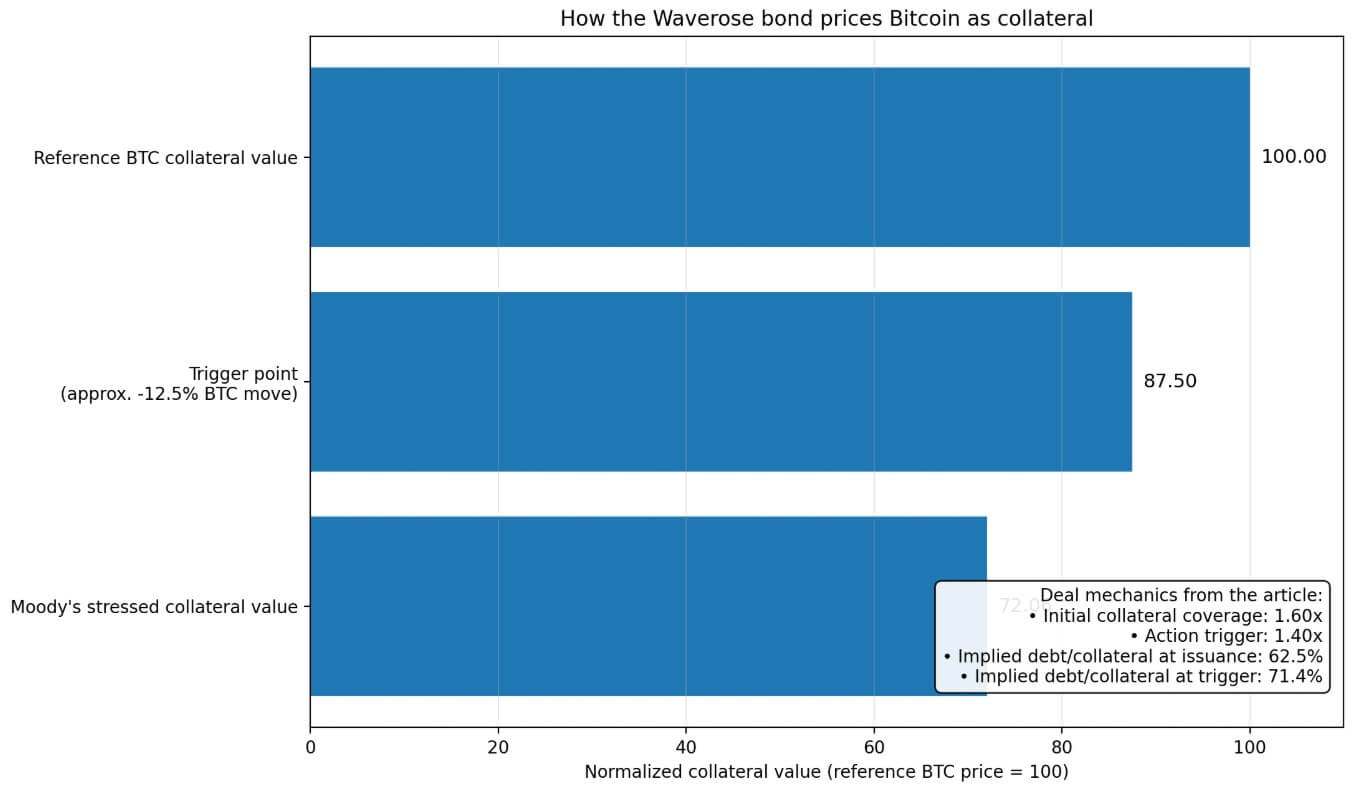

These numbers set the situations below which conventional finance agreed to work with Bitcoin in any respect: 72.06 cents of credit score for each greenback of collateral worth, a two-day publicity window to behave on worth strikes, and 1.60x preliminary collateral protection, which forces motion when it drops to 1.40x.

Bitcoin has spent years auditioning for legitimacy as a retailer of worth, a company treasury reserve, and an ETF asset. The New Hampshire deal factors to Bitcoin as collateral.

Collateral is the place an asset earns credit score utility, one thing establishments can borrow towards inside buildings that credit score markets can perceive, worth, and, when vital, liquidate quick. That’s the line Bitcoin simply crossed.

Why this issues: That is the primary time Bitcoin has been formally translated into credit score phrases that public markets perceive. As a substitute of being held or traded, BTC is now being assigned a borrowing worth, a liquidation threshold, and a stress worth, turning it from an asset into usable monetary collateral. That shift opens a brand new supply of liquidity for holders, but in addition introduces a system the place worth drops can set off automated promoting throughout a number of buildings directly.

The opening worth of belief

The Waverose construction is a taxable conduit income bond.

New Hampshire’s position ends on the conduit, and bondholders carry all loss danger. That is limited-recourse, institutional plumbing.

Two issues comply with from that construction. First, it retains danger quarantined: if the collateral breaks down, bondholders soak up the loss. Second, it lays out the exact phrases on which conventional finance determined Bitcoin might enter the credit score system.

At 1.60x preliminary collateral protection, the bond begins with debt equal to about 62.5% of collateral worth. The 1.40x set off, at which automated motion kicks in, implies a debt of roughly 71.4%.

The construction hits its wire journey when BTC falls by roughly 12.5% from issuance pricing, a transfer Bitcoin has executed routinely.

Moody’s harassed the collateral worth at 72.06% of the market worth. Mapped to Bitcoin’s Apr. 1 worth within the $68,000 zone, the stress zone lands close to $49,600.

Customary Chartered put its near-term bear case for Bitcoin at $50,000, and the standard finance companies calibrated their first public finance haircut on Bitcoin nearly precisely on prime of a draw back path that one of many world’s largest banks nonetheless considers reachable.

From owned to pledged

New Hampshire arrived alongside two different current strikes pointing in the identical route.

In February, S&P assigned the first-ever score to a structured finance transaction backed by Bitcoin. The transaction was the Ledn Issuer Belief 2026-1, with roughly $199.1 million in loans secured by 4,078.87 BTC, carrying a good market worth of roughly $356.9 million, implying an LTV of about 55.8% at inception.

In March, Higher and Coinbase launched what they referred to as the primary crypto-backed conforming mortgage, by which a borrower pledges $250,000 in BTC to fund a $100,000 down cost, whereas the primary lien stays Fannie Mae-backed.

Bitcoin obtained three credit score wrappers in roughly six weeks, every with totally different haircuts, liquidation mechanics, and regulatory constraints. Collectively, they describe a course of by which Bitcoin enters credit score markets via a number of doorways directly, and people doorways are edging nearer to strange family finance.

| Construction | Date | Wrapper sort | Collateral / pledge | Haircut / Lationale | Who bears danger | Why it issues |

|---|---|---|---|---|---|---|

| Waverose / New Hampshire | Mar. 31, 2026 | Taxable conduit income bond | Bitcoin pledged as collateral for bonds secured by a mortgage to NH CleanSpark Borrower Belief 2026-1 | Moody’s harassed collateral at 72.06% of market worth; 1.60x preliminary collateral protection; motion triggered at 1.40x; implied debt-to-collateral begins round 62.5% and rises to 71.4% at set off | Bondholders soak up losses if collateral fails; no New Hampshire public funds pledged | Reveals Bitcoin coming into public-finance-adjacent credit score as rated collateral, not simply as an owned asset |

| Ledn Issuer Belief 2026-1 | February 2026 | Structured finance / ABS | Roughly $199.1 million in loans secured by 4,078.87 BTC with honest market worth of about $356.9 million | About 55.8% LTV at inception | Traders within the structured-finance deal; danger tied to collateral, operations, and liquidation mechanics | Marks Bitcoin’s entry into rated structured finance |

| Higher / Coinbase mortgage product | March 2026 | Crypto-backed conforming mortgage / down-payment mortgage | Borrower pledges $250,000 in BTC to acquire a $100,000 mortgage for a house down cost, whereas the primary lien stays Fannie Mae-backed | Instance implies a 40% advance price on pledged BTC | Danger sits with the crypto-backed mortgage construction, whereas the primary mortgage stays individually conforming/Fannie-backed | Pushes Bitcoin collateral nearer to family finance and mainstream mortgage plumbing |

The US municipal market carried $4.4 trillion in excellent bonds as of the fourth quarter of 2025. Households held 48% straight and about 21% via mutual funds.

Munis occupy a selected psychological slot in American financial savings tradition, sitting the place advisors park cash for purchasers who need security adjoining to tax effectivity.

The Waverose bond lands within the taxable conduit nook. Taxable muni issuance ran solely about $33 billion in 2025, lower than 6% of the market whole. At $100 million, this deal represents roughly 0.0023% of the excellent muni market.

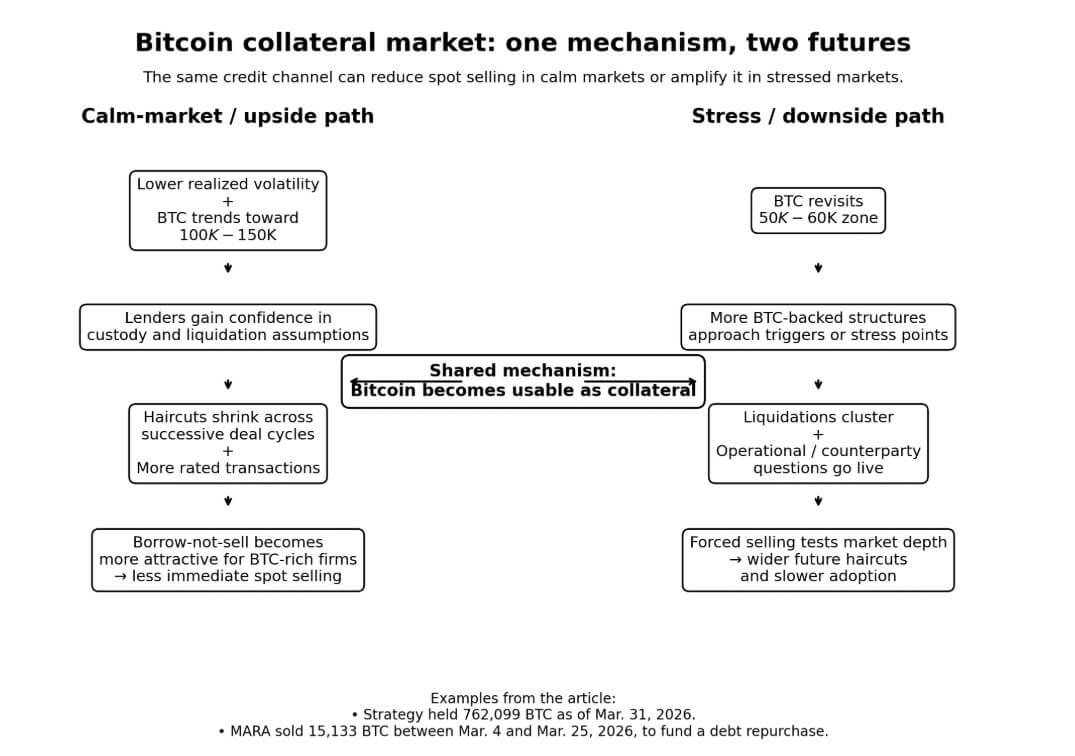

One mechanism for 2 potential futures

For Bitcoin holders and treasury-heavy companies, collateral utility cuts in reverse instructions relying on the place the value goes.

Technique held 762,099 BTC as of Mar. 31. Between Mar. 4 and 25, MARA bought 15,133 BTC for about $1.1 billion to fund a debt repurchase, which had been outright spot gross sales to cowl a stability sheet obligation.

A functioning BTC-collateral market sits between the 2 postures of full accumulation and outright liquidation, whereas offering credit score towards reserves that lets holders elevate capital whereas maintaining their Bitcoin place.

Constancy famous in March that public corporations and ETFs collectively maintain roughly 12% of Bitcoin’s circulating provide, and that 2025 was Bitcoin’s least risky yr on file, based mostly on annualized realized volatility.

If that holds and Bitcoin trades towards the $100,000-$150,000 vary Bernstein projected for late 2026, the collateral channel turns into genuinely engaging. BTC-rich companies carry massive reserves at decrease realized volatility, lenders construct confidence in liquidation assumptions, and the haircut required to entry credit score shrinks throughout successive deal cycles.

Every rated transaction provides information to Bitcoin’s almost empty monitor file as pledged collateral. A second deal, a 3rd, a cluster, and the pricing of belief begins to compress.

The bear case runs via the wrong way of the identical mechanism. Bitcoin revisiting $50,000, close to Customary Chartered’s draw back projection and near the Moody’s stress zone from present costs, turns the operational query stay.

Corporations begin to wonder if the liquidation mechanics work cleanly when each BTC-backed construction must exit directly.

S&P’s score work on the Ledn ABS flagged operational and counterparty danger, occasion danger, and liquidation mechanics because the core uncertainties for Bitcoin-backed credit score. It famous the market’s capacity to soak up compelled promoting from a number of buildings tripping triggers inside the identical worth window.

A construction that reduces compelled promoting in calm markets can focus it in turbulent ones. That’s the inherent geometry of collateralized credit score, and Bitcoin’s volatility makes the geometry sharper than it might be for any standard pledged asset.

The primary model of Bitcoin-backed public finance is small, speculative-grade, and constructed for taxable conduit territory. The structure is constrained as a result of these constraints had been the one phrases on which the credit score system would have interaction.

What Moody’s launched on Mar. 31 was a pricing schedule for Bitcoin’s entry into credit score markets: the situations below which bond traders set for accepting it as collateral.

Future offers will probably be negotiated on that schedule, tightening haircuts if volatility falls, widening them if it rises, testing totally different custody preparations, and pushing towards the investment-grade boundary.

Every iteration provides institutional reminiscence to a market that presently has nearly none.

Bitcoin took years to turn into one thing establishments might purchase via regulated channels. Turning into one thing they’ll lend towards will comply with the identical logic of incremental, conditional progress, constructed on an accumulating monitor file.