Crypto change Coinbase World has launched a mortgage construction with Higher Dwelling & Finance that lets certified debtors pledge digital property held in Coinbase accounts to fund down funds on normal conforming mortgages designed in accordance with Fannie Mae pointers.

In accordance with Coinbase, the construction permits debtors to pledge digital property corresponding to Bitcoin ($BTC) or $USDC ($USDC) as collateral for a separate mortgage used to fund the down cost, whereas the first mortgage stays an ordinary, Fannie Mae–backed mortgage. Higher will originate and repair the mortgages.

When rolled out, the brand new improvement may mark a shift in how crypto property are utilized in US housing finance, extending their function from qualifying property in underwriting to a extra direct element of mortgage financing.

The information follows earlier regulatory alerts to combine crypto into mortgage frameworks. In June, the US Federal Housing Finance Company directed Fannie Mae and Freddie Mac to arrange proposals to acknowledge cryptocurrency as an asset in mortgage danger assessments with out requiring conversion to US {dollars}.

It additionally builds on a collection of developments integrating crypto into dwelling lending, with lenders like Newrez and Fee lately recognizing crypto holdings in underwriting, signaling a broader push to embed crypto throughout the mortgage stack.

Cointelegraph reached out to Fannie Mae for extra data however didn’t obtain a response earlier than publication.

Pledging crypto for down funds comes with added dangers

In accordance with Coinbase, debtors would take out an ordinary conforming mortgage whereas utilizing a separate mortgage secured by crypto holdings to cowl the down cost.

The setup permits patrons to retain publicity to digital property, however replaces upfront money with further debt.

Associated: Crypto mortgages in US face valuation dangers, regulatory uncertainty

Coinbase mentioned the mannequin introduces constraints tied to pledged property, with debtors unable to commerce collateral whereas it’s locked.

The corporate mentioned market volatility alone doesn’t set off margin calls so long as debtors proceed making funds, and mortgage phrases stay unchanged as soon as the mortgage is energetic.

The mannequin additionally introduces new dangers tied to the pledged property. Whereas worth swings don’t instantly have an effect on the mortgage, they could nonetheless affect borrower danger publicity and monetary selections over time.

Lenders have been step by step integrating crypto into mortgage underwriting

The brand new improvement follows a number of US lenders that lately included crypto property into mortgage processes.

On Jan. 17, mortgage servicer Newrez mentioned it might permit debtors to make use of $BTC, Ether (ETH), crypto ETFs and stablecoins as qualifying property in underwriting, with out requiring liquidation.

On Feb. 23, mortgage lender Fee launched its RateFi program, which permits verified crypto holdings to rely towards reserves and, in some instances, revenue. Nonetheless, debtors are nonetheless required to transform their crypto into money for down funds and shutting prices.

Ex-Congressman Ryan frames crypto as a housing instrument

Forward of the rollout, Cointelegraph’s Turner Wright spoke with former Ohio Consultant Tim Ryan, a member of Coinbase’s advisory council who has targeted on middle-class affordability, together with housing.

Ryan forged mortgage financing as a sensible, real-world use case for crypto, arguing that digital property can unlock wealth for early buyers and assist tackle one of many greatest boundaries to homeownership — the down cost.

“Digital property have a spot for working-class individuals… all the best way right down to getting a house,” Ryan mentioned. “To see the business transfer into… the housing sector… is a extremely big deal.”

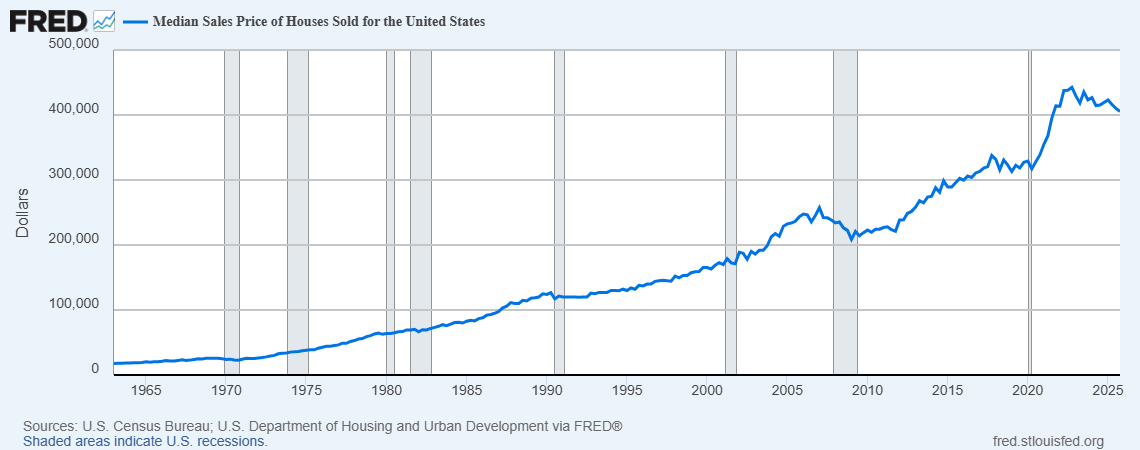

Affordability stays a significant problem for US homebuyers. Regardless of slower exercise tied to low stock and elevated mortgage charges, the common dwelling worth nonetheless exceeded $405,000 within the fourth quarter.

The median dwelling worth has come down from its 2022 peak however stays elevated relative to incomes. Supply: Federal Reserve Financial institution of St. Louis

A 20% down cost, typically required to keep away from non-public mortgage insurance coverage, would nonetheless value patrons greater than $80,000, a hurdle that might be much less difficult now for crypto buyers.

Further reporting by Sam Bourgi and Turner Wright.

Associated: Bitcoin ‘compression’ final result could ship $BTC to $80K: Analyst

Journal: No one is aware of if quantum safe cryptography will even work