Most merchants insist that that is the worst Bitcoin halving cycle in historical past, however knowledge signifies the comparability might come from a skewed place to begin.

These issues have emerged as a result of Bitcoin’s ($BTC) efficiency since its fourth halving on April 19, 2024. The crypto asset now trades at $59,400, under the roughly $64,000 value it held on the day of the halving.

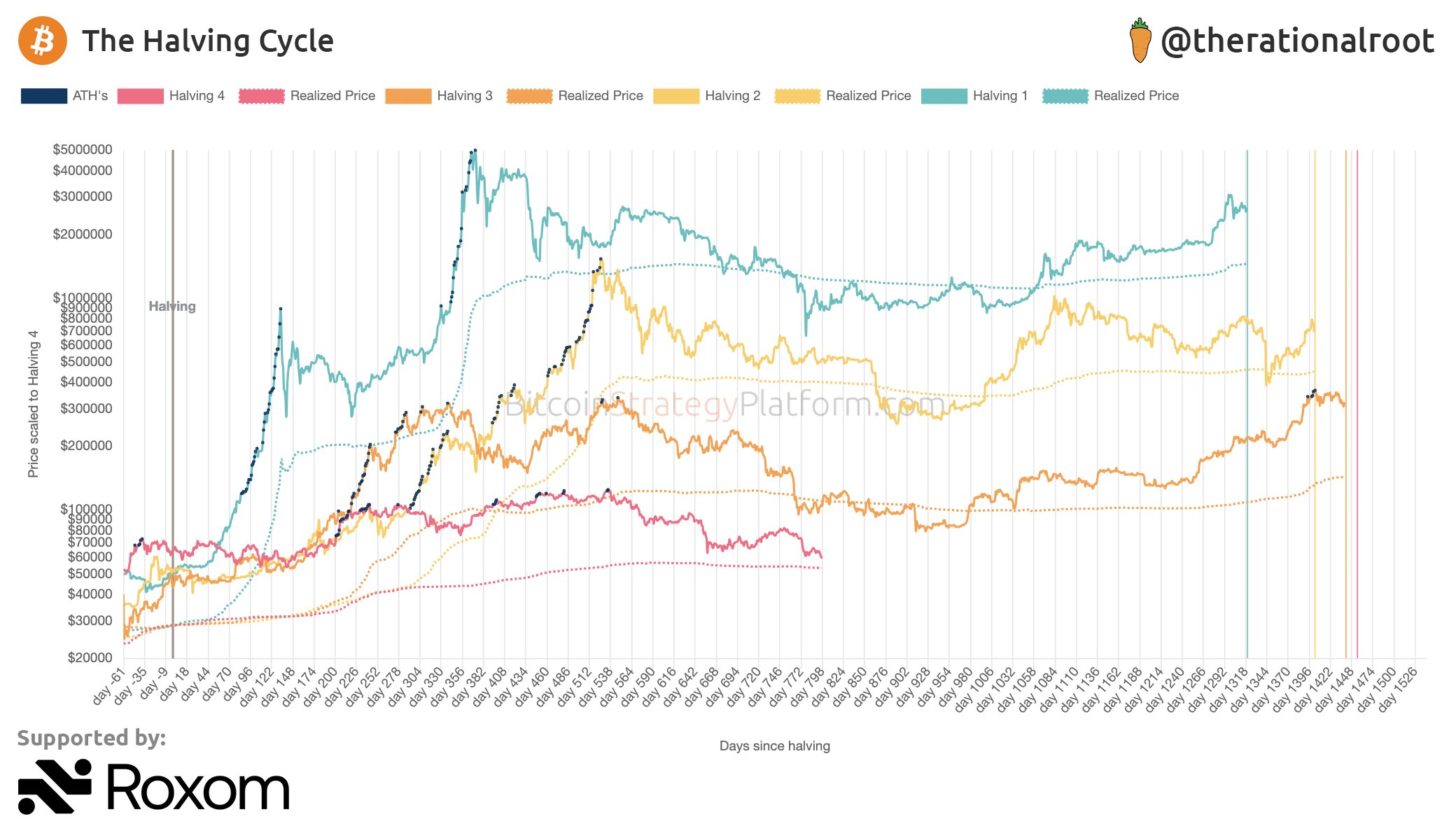

Bitcoin Halving-Day Consumers Nonetheless Underwater

This means that greater than 800 days later, buyers who purchased Bitcoin on halving day are nonetheless sitting at a loss. That is the primary time in Bitcoin’s historical past that halving-day patrons have remained underwater this far right into a cycle. In each earlier cycle, they have been already in revenue by this stage.

Bitcoin’s drop from its peak has additionally added to the issues. Particularly, the crypto firstborn has fallen about 53% from its all-time excessive of round $126,000, reached on Oct. 6, 2025.

Now, whereas this decline continues to be smaller than the drops of greater than 77% that adopted the market peaks in 2018 and 2022, Bitcoin has not delivered the sturdy positive aspects the market recorded in earlier cycles.

Skewed Beginning Level

Nonetheless, the halving date is a skewed place to begin as a result of this cycle started beneath situations Bitcoin had by no means skilled earlier than. Notably, $BTC had already reached a new all-time excessive of $73,800 on March 12, 2024, greater than a month earlier than the fourth halving.

This was a significant change from earlier cycles. In earlier halvings, Bitcoin had not but moved above the earlier bull market’s peak by the point the halving happened. In consequence, on the halving day, the market nonetheless had room to climb earlier than reaching new highs. This cycle adopted a totally completely different path.

A significant motive for the distinction was the launch of U.S. spot Bitcoin ETFs in January 2024. These funds attracted huge institutional demand nicely earlier than the halving decreased Bitcoin’s new provide. On the halving day, they’d already attracted $12.3 billion in cumulative internet inflows.

This early shopping for pushed Bitcoin’s value a lot larger earlier than the halving even arrived, creating an unusually excessive place to begin.

Realized Worth Presents a Higher Approach to Examine Cycles

Many analysts think about realized value a greater benchmark as a result of it doesn’t react as rapidly to single occasions. Particularly, realized value measures the common value of all cash in circulation primarily based on the value at which every coin final moved on-chain.

Since realized value modifications step by step as buyers purchase and promote Bitcoin, it’s much less affected by main occasions resembling ETF approvals. This makes it a extra steady method to examine completely different market cycles with out the distortion created by Bitcoin’s unusually sturdy rally earlier than the halving.

Bitcoin’s realized value at the moment stands at $53,197, whereas the spot value is round $59,400. Meaning the spot value trades at a premium of roughly 10% above the realized value, one of many smallest gaps seen throughout this cycle.

In previous cycles, Bitcoin reached main market bottoms when the spot value moved this near the realized value, together with the lows recorded in 2015, late 2018 into 2019, and 2022.

Bitcoin Realized Worth Nonetheless Exhibits This Has Been a Weak Cycle

Nonetheless, even after eradicating the impact of Bitcoin’s early rally, realized value doesn’t make a bullish case for this cycle. As a substitute, it nonetheless factors to weaker efficiency than earlier halving intervals.

Throughout this cycle, the Bitcoin market value by no means moved far above realized value the way in which it did throughout the main bull market peaks of 2013, 2017, and 2021.

In these earlier cycles, heavy hypothesis pushed Bitcoin’s market worth a number of occasions above the mixed value foundation of all cash. Such a spot by no means developed this time, even when Bitcoin reached its document excessive in October 2025.

The smaller hole between spot value and realized value suggests this market has behaved otherwise from earlier ones. The present cycle has been formed by regular institutional shopping for by spot Bitcoin ETFs as a substitute of being pushed primarily by retail hypothesis.

It’s nonetheless too early to know whether or not it will lead to a smaller market backside or just a quieter bull market. Nonetheless, whereas utilizing realized value as a substitute of the halving-day value removes the distortion brought on by ETFs, it nonetheless signifies that the cycle has been worse than others at related intervals.